- Quick take

- 15 February 2023

- United States

US retail sales surge on stark weather contrast

US retail sales jumped 3% month-on-month in January as warm weather encouraged people to go out and spend after harsh conditions depressed activity in December. Household incomes remain under pressure and with weather patterns normalising a correction is likely in February

A strong start to the year with broad-based gains

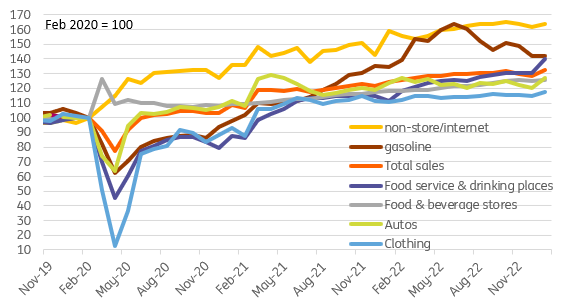

As suspected, we have a very strong US retail sales report for January with headline sales up 3% MoM versus the 2% consensus. This is the fourth biggest MoM rise in retail sales over the past 20 years. Importantly, the "control" group which excludes volatile categories and better correlates with broader consumer spending was also much stronger than anticipated, rising 1.7% MoM versus the 1% consensus.

We knew autos would be strong (+5.9% MoM) given unit volume figures jumped 18%, but there were huge gains elsewhere with clothing up 2.5% MoM, general merchandise up 3.2% (within which department stores saw a 17.5% MoM jump) and eating & drinking out, which surged 7.2%. The one real surprise was the flat gasoline station sales despire prices having risen by more than 4%.

US retail sales levels

Weather played a strong role and the risk of a February correction is high

Much of this will be down to the stark contrast between the weather in December versus January. Remember that December experienced very cold temperatures with heavy snowfall disrupting travel in many parts of the nation. This also depressed spending with November and December both posting 1.1% MoM declines. Therefore we should expect a rebound in January anyway, but then very warm temperatures providing an additional stimulus that tempted more people to leave their homes and spend.

However, we have to be a little cautious that with weather patterns returning to more seasonal norms in February we could get a significant correction next month - especially with household finances remaining under pressure from high inflation and slowing wage growth. Consequently, today's numbers back the case for a March and probably a May hike, but it shouldn’t push the case for Fed tightening beyond that.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more