US production boosts case for 4% GDP growth

Consumer spending looks set to contribute significantly to third quarter GDP growth, but with manufacturing showing signs of stabilising and construction continuing to post robust gains then we could be looking at something close to a 4% annualised increase

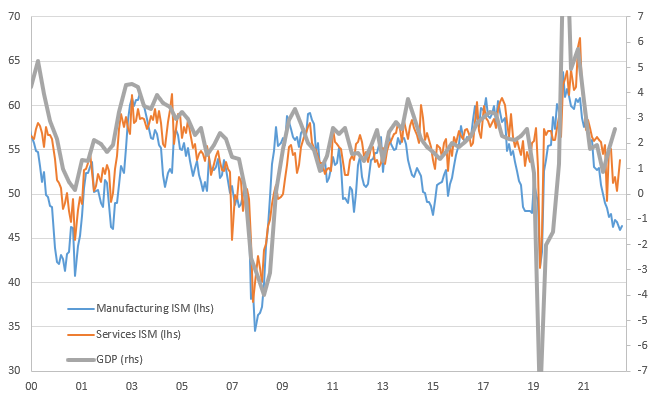

Manufacturing is stabilising after 11 months of contraction

The US ISM manufacturing index has improved to 49.0 from 47.6 (consensus 47.9), although we have to remember it remains below 50, thereby indicating the sector continues to contract, albeit at a slower pace than last month. Furthermore, we have to remember that this is the 11th consecutive sub 50 reading so looking at it cumulatively we are at pretty weak levels of activity. Nonetheless, there are areas of very positive news with the details showing production actually broke above 50 to stand at 52.5, which is the best reading since July 2022 while employment also posted positive growth with an index level of 51.2 – the highest print since May. New orders improved to 49.2 from 46.8 with export orders at 47.4 versus 46.5 previously – but again as these are below 50 it merely signals the rate of contraction is moderating.

ISM indices & GDP growth

There is more positive news on the inflation front with prices paid slipping to 43.8 from 48.4. We had feared that rising energy costs would lead to a spike in this metric, but it appears that there is enough moderation in costs elsewhere to offset it. Consequently we see a story that points to stabilising activity in the manufacturing sector with limited price pressures, which is encouraging for the Federal Reserve’s soft landing thesis.

Construction continues to see robust increases in spending

At the same time we have August construction data which shows spending rose 0.5% month-on-month, as expected, with a 0.6% gain in residential activity and a 0.4% increase in non-residential construction spending. It is worth noting that construction activity tied to manufacturing is up 65.5% year-on-year with the CHIPS Act and FABS Act to stimulate semi-conductor production in the US gaining particular traction. So, with consumer spending looking strong in the third quarter, construction making robust gains and manufacturing showing signs of stabilisation, it all seems to tally with the prospect of a very healthy 3.7% annualised growth rate for third quarter GDP as we are forecasting. However, the risks appear skewed to the upside and a 4% figure is entirely possible.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap