- Quick take

- 14 January 2022

- United States

US manufacturing weakness adds to growth concerns

Manufacturing output surprisingly declined in December, which suggests supply chain strains and worker shortages continue to hold the economy back. Record Covid case numbers and enforced isolation will only intensify these problems in the near-term

Manufacturing constrained by production bottlenecks

Following on from the shock December retail sales plunge we see manufacturing output also fell in December. Output contracted 0.3% month-on-month versus expectations of a 0.3% gain that was based on the decent ISM and regional manufacturing numbers. The weakness was primarily in auto-related output, which fell 1.3%, presumably on lingering supply chain problems holding back output given strong demand for vehicles. However, even excluding this key component, non-auto manufacturing still fell 0.2% MoM.

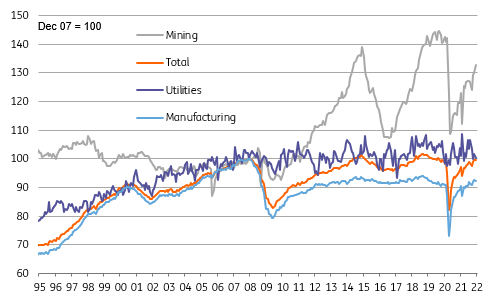

Industrial production levels

Fed focused on inflation... assuming Omicron wave subsides

Utilities actually held up better than thought. Output was down “only” 1.5% despite the really warm weather that would have dampened demand for heating. Mining output then rose 2% led by a 3.7% increase in oil & gas well drilling. Putting it altogether this leaves industrial production posting a 0.1% MoM contraction in December versus expectations of a 0.2% gain.

Unlike the retail sales report, this won’t materially alter GDP expectations given November's growth rate was revised a little higher. Nonetheless, it provides more evidence to suggest a loss of economic momentum in December that likely continues into January where worker absences could curtail output growth.

Inflation though is the Fed’s key concern right now and so long as Omicron case numbers start to subside in the weeks ahead, prompting hope for a rebound in activity in 2Q, the market is likely to continue to back the March rate hike view.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more