Soft US manufacturing and construction numbers emphasise the dependency on services

With the manufacturing ISM pointing to contraction and construction spending faltering, Monday’s data highlights how dependent the US economy is on the ongoing strength in consumer demand for services

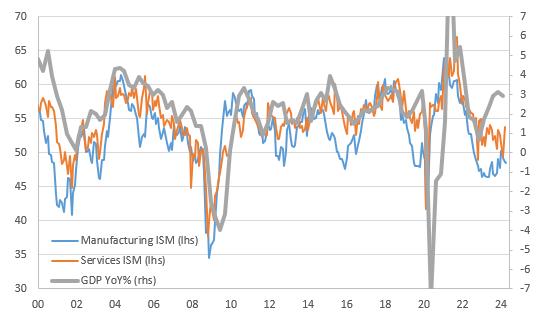

ISM components highlight the problems for US manufacturing

Today's US data has come in on the softer side of expectations with the June ISM manufacturing index dipping to 48.5 from 48.7. The consensus was looking for a modest recovery to 49.1. This is the 19th sub-50 reading, thereby indicating contraction in the past 20 months, with only March breaking the trend with a 50.3 print. The chart below shows that the ISM indices used to be an excellent lead indicator for judging turning points in the economic cycle, but for now, the economy continues to perform strongly despite the apparent softness in the surveys.

US GDP growth YoY% versus the ISM indices

The details show production dropped to 48.5 from 50.2 (6M avg of 50.6), with new orders at 49.3 (6M average of 49.5). Employment fell to 49.3 from 51.1 (6M average of 48.2). With the big three components all in contraction territory it highlights how the manufacturing sector continues to struggle and will not be contributing meaningfully to economic growth this year. The one positive story is that inflation pressures continue to subside, with the prices paid component dropping to 52.1 from 57.0 versus a 6M avg of 55.2.

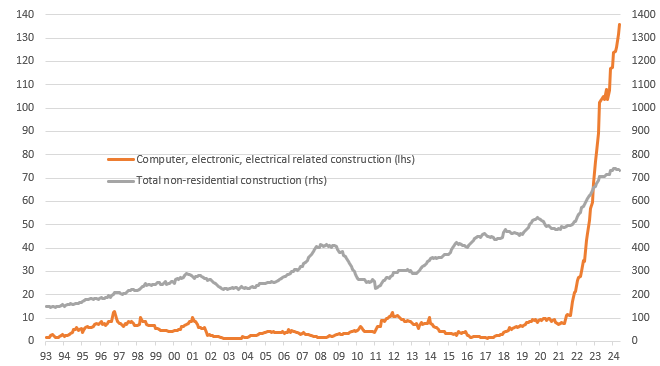

Financing issues constrain construction spending

Construction spending fell 0.1%MoM rather than rising 0.2% as expected, although April's number was revised up quite a bit to +0.3%MoM growth. Both residential and non-residential construction spending fell in May. Issues with financing construction activity and weak demand due to high borrowing costs are likely to mean construction activity also softens through the year.

Furthermore, the chart below shows that investment tied to the CHIPS Act, which was designed to incentivise the re-shoring of semiconductor chip manufacturing, is the primary driver of construction spending in the US right now. The money is not infinite though, and we expect growth to subside through the second half of the year. Putting the manufacturing and construction numbers together emphasises how reliant the US is on the consumer to keep the service sector momentum going.

Non-residential construction spending ($bn)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap