US industry posts solid gains, inflation expectations plunge

Another respectable industrial production report while the University of Michigan reported a big plunge in inflation expectations. All this should be music to the ears of the Federal Reserve as it seeks a soft landing for the economy and a return to 2% inflation

Decent industrial output, but strike action could weigh in coming months

As with the retail sales report, the US industrial production number beat expectations in August, but the downward revisions to July means that on balance the level of activity is broadly in line with what was expected. This has been a bit of a trend of late with big prints subsequently getting some chunky downward revisions, be it in manufacturing, consumer spending, jobs or GDP.

In terms of today’s numbers, US industrial production rose 0.4% in August versus the 01% expected, but there was a 0.3pp downward revision to July's growth (from 1% to 0.7%). Manufacturing rose 0.1% as expected, but there was a 0.1pp downward revisions to July from 0.5% to 0.4% growth. Auto output fell 5% month-on-month after a 5.1% jump the previous month with manufacturing ex vehicles rising 0.7%, led by a 2% jump in machinery manufacturing. Outside of manufacturing, which makes up 74% of total industrial output, utilities output rose 0.9% while mining increased 1.4%.

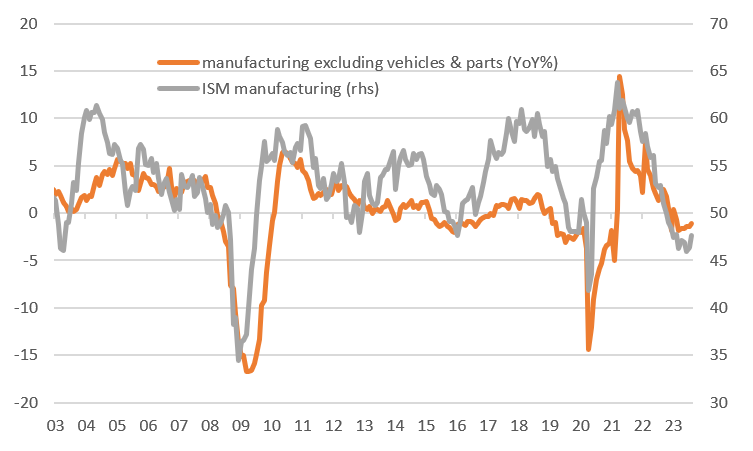

On balance the report is OK and is stronger than what is implied by the manufacturing ISM report, which has been in contraction territory for 10 consecutive months. However, auto output is up near record highs. Strip this out and the chart below shows there is a much tighter relationship between the ISM and non-auto related manufacturing.

Today’s report won’t swing the Fed debate in either direction meaningfully. The key story for manufacturing next month will be how much the UAW strike action hits output. So far it is starting out modestly with just 12,700 on strike, but could quickly escalate and hit output hard.

ISM manufacturing index versus non-auto manufacturing output (YoY%)

US consumer inflation expectations fall sharply

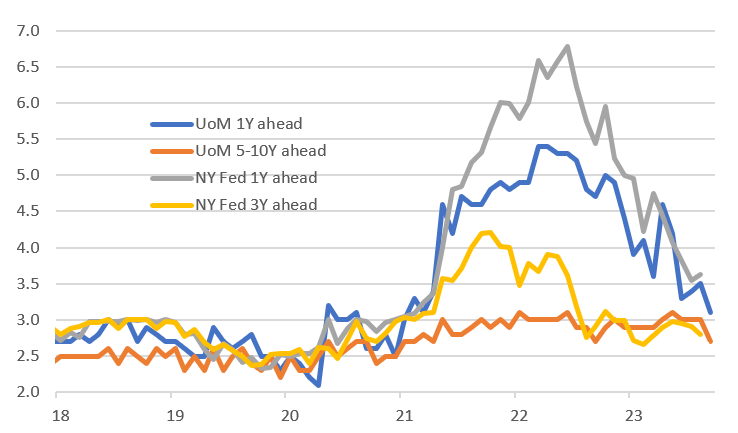

University of Michigan confidence fell more than expected to 67.7 from 69.5 (consensus 69.0). The perception on current conditions fell six points while expectations rose 0.8 points. Remember this index is much more responsive to inflation-related issues while the Conference Board measure of confidence is more reflective of the labour market (hence why the Conference Board suggests everything is great, with unemployment below 4%, yet the University of Michigan measure of sentiment suggests the world is on the cusp of falling apart).

Rising gasoline prices are the likely culprit depressing today's report as households feel the hit to spending power it generates elsewhere. Yet, rather bizarrely, we have some big declines in inflation expectations which should be music to the ears of the Fed. 1Y inflation expectations are down to 3.1% from 3.5% – it is actually below the current level of inflation – while 5-10Y expectations dropped from 3% to 2.7%. Both are really big surprises, but the usual caveat applies that they use fairly small sample sizes and things can swing. Nonethless, on balance this is further evidence that backs the Federal Reserve's claims that it can achieve a soft landing for the economy while returning inflation sustainably to target.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap