UK inflation surprise boosts chances of Bank of England pause

We're still tempted to say the Bank of England will hike rates tomorrow, and some of the downside surprise in services inflation is down to volatile travel categories. But it's a close call, and both wage and inflation data suggest the end of the current tightening cycle is very close to its conclusion

Thursday’s Bank of England meeting just got a lot more interesting.

August’s inflation data has come in well below expectations, and core CPI now sits at 6.2%, down from 6.9%. Both we and the consensus had expected this to dip just a tenth of a percentage point. More importantly, services inflation – which we know is one of the key metrics for the BoE – fell from 7.4% to 6.8%. That’s comfortably below the Bank’s most recent forecast of 7.2% for August.

Admittedly, these numbers do deserve a bit of caution. The majority of that fall in services inflation can be put down to airfares and package holidays. Both of these saw prices fall in level terms, which is highly unusual for August. These moves don’t tell us a huge deal about “persistence” in inflation, in the same way that July’s surprise pick-up in services inflation was down to an unusual spike in social rents. The Bank of England will probably treat both July’s increase and August’s fall in services CPI with a light pinch of salt given the volatility we’re seeing.

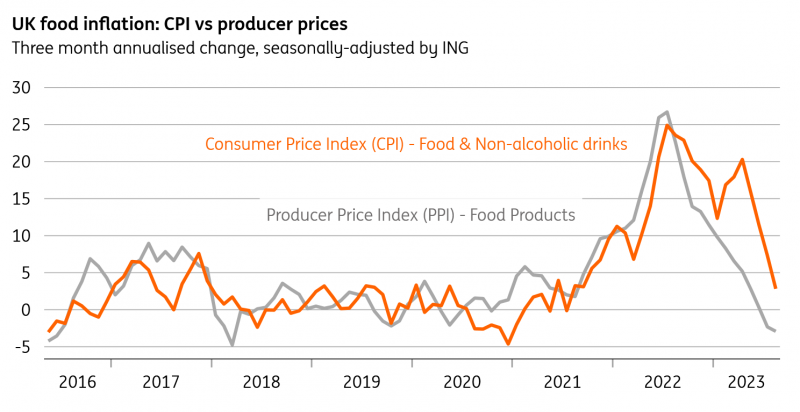

That said, we are clearly seeing disinflation across a range of categories, particularly for goods. Household goods and vehicles, both major contributors to core inflation during the supply chain issues, have seen inflation rates collapse over recent months. Food inflation, though less relevant to BoE decision-making, is also coming down quickly. The recent falls in the level of producer prices suggest food inflation will end the year below 10% from 13.6% now.

UK food inflation is falling quickly, inline with producer prices

All of this makes tomorrow’s BoE meeting a much closer call. We’d already been flagging the risk that the Bank could opt to pause this week while still keeping the door open to another hike in November, and that scenario has now become more realistic. Today's downside miss on services inflation followed some slightly dovish news on wage growth last week, where there were hints that this may finally be starting to ease – or is at least reaching a peak. That same report also showed that the jobs market is cooling noticeably.

It's a very close call, but we’re still tempted to say the Bank will follow through with a hike tomorrow. But we could get a couple more members voting for a pause, and either way a rate hike tomorrow – if it comes – is likely to be the last.

BoE officials have very clearly been laying the ground for a pause over recent weeks, and that should be aided by further falls in services inflation over the coming months. Lower gas prices are taking a lot of the pressure off service-sector businesses to raise prices. We suspect services inflation will end the year below 6% and fall further through the first half of next year. Rate cuts could begin around the middle of 2024.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap