US housing feels the squeeze from high mortgage rates

A tripling of US mortgage rates constrained both the demand and supply of housing, leaving existing home sales at post-GFC lows. Mortgage rates will rise further in the wake of the market's reaction to yesterday's Fed forecasts, further constraining activity

Market acknowledges the risk of a final hike, but it will depend on the data

The Fed's messaging of higher for longer interest rates has been taken on board by financial markets, with the dollar strengthening and the yield curve shifting higher in the wake of yesterday's decision. Nonetheless, the market remains somewhat sceptical on the prospect of the final 25bp interest rate rise that the Fed's forecasts signalled for this year, with the pricing for November's FOMC meeting only being 8bp with 13bp priced by the time of the December meeting.

The jobs market remains tight, as highlighted by low jobless claims numbers today, but we continue to believe that core inflation pressures will slow meaningfully, the economic outlook will soften, and the Fed won't end up carrying through. The jobs market is always the last thing to turn lower in a downturn and there are areas of more obvious weakness.

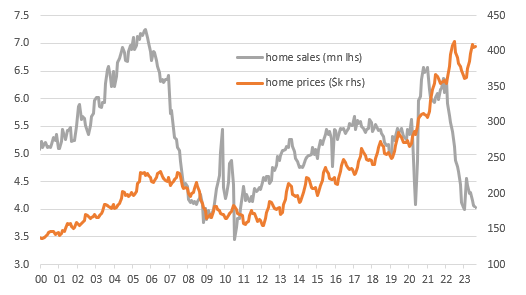

For example, US existing home sales fell 0.7% MoM in August to a level of 4.04mn rather than rising the 0.7% MoM as the market expected. This is due not only to weakness in demand but also a complete collapse in properties available for purchase. The affordability issue is front and centre here, with prices having risen nearly 50% nationally during the pandemic, but demand has obviously been crushed by the fact that mortgage rates have tripled since the Federal Reserve started hiking interest rates. But this surge in borrowing costs is constraining the supply of homes for sale as well - people who are locked in at 2.5-3.5% mortgage rates cannot afford to give them up. They can't take the mortgage with them when they move home, so even if you downsize to a smaller, cheaper property, you are, in all likelihood, going to end up paying a higher monthly dollar mortgage payment.

We're in a crazy-sounding position

Consequently, we are in a crazy-sounding position whereby the number of housing transactions is on a par with the lows seen during the global financial crisis, yet home prices are rising. This should be a boon for home builders, but note the big drop in sentiment and housing starts seen earlier in the week. The drop-off in prospective buyer traffic is making builders cautious. Mortgage rates at 7%+ will obviously do that over time, but it may be another sign of the household sector starting to pull back at the margin now that the Fed believes pandemic-era savings are close to being exhausted.

Existing homes sales transactions and home prices

Leading index still indicates recession can't be ruled out

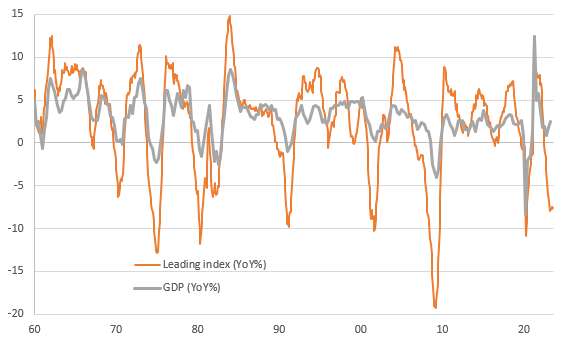

Meanwhile, the US leading economic indicator, which combines a range of other numbers, including jobless claims, orders, average work week, the yield curve and credit conditions, posted its 17th straight monthly decline. As the chart below shows, the index at these sorts of levels has been a clear recession indicator in the past, but for now, GDP growth is strong.

Leading index versus GDP (YoY%)

Our view remains that this strength in activity has been caused primarily by households running down pandemic-era accrued savings aggressively and borrowing more on credit cards. But with savings obviously being finite - note the Fed's Beige Book citing evidence of the "exhaustion" of these savings - and consumer credit harder to come by and certainly less affordable than it was, the cashflow required to finance ongoing increases in spending will have to increasingly come from rising real income growth. Rising gasoline prices will erode spending power while student loan repayments, strikes and the prospect of a government shutdown will add to the financial stresses on millions of households, so we will need to see substantial wage increases for everyone - not just auto workers - to keep this growth engine firing.

Given this situation, we not only think the Fed will leave rates at their current levels, we also see the potential for more rate cuts next year than the 50bp currently being signalled by the Federal Reserve.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap