- Quick take

- 21 May 2021

- United Kingdom

UK: Solid PMIs round off buoyant week of data

UK PMIs are the latest indicators to suggest the economy is already in a better place than after the first wave last summer. We expect around 5% growth in the second quarter and think the economy will be just shy of, or maybe even back to, pre-virus levels by the end of the year

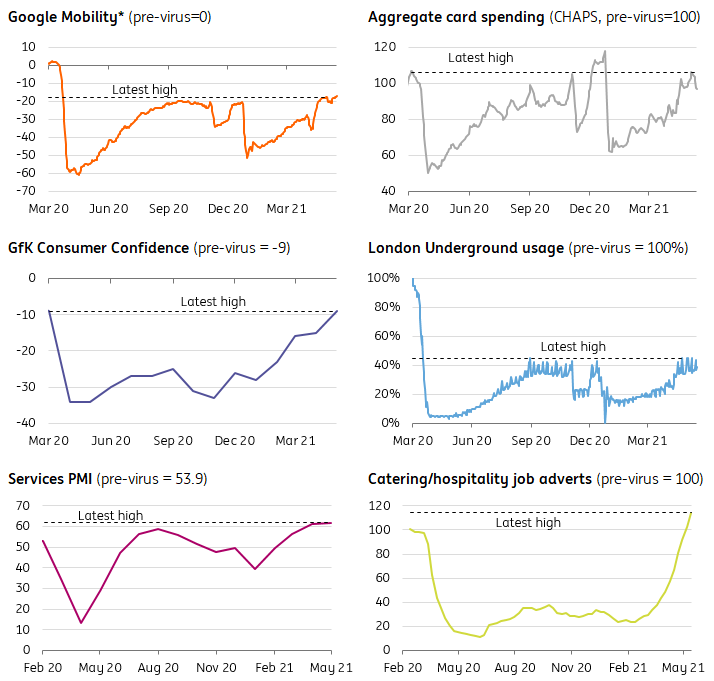

The latest rise in the UK PMIs rounds off what has been a pretty buoyant week for UK data. While the lofty level of the services index, now at 61.8, heavily reflects the recent reopenings, it also paints a picture of consumers and businesses that are more confident in the forthcoming recovery. Most data points – from consumer confidence to transport usage – are now back to, or exceeding, the levels we saw last summer when restrictions were at their lowest.

Here are a few things that stand out from the latest PMIs:

Hiring is bouncing back quickly

Firstly, hiring is clearly picking up quickly. We know from Adzuna job advert data that the number of adverts in the hardest-hit catering/hospitality sector are now above pre-virus levels, while the PMIs noted the highest employment reading since 2014, putting some pressure on salaries.

While neither measure is the same as saying that employment is back to pre-virus levels, it does suggest that the recovery in the jobs market is likely to be faster than after past crises, despite the forthcoming rise in unemployment we’re likely to see when the furlough scheme unwinds. Anecdotally, hospitality firms are struggling to meet hiring requirements, partly because of a sharp fall in EU workers in the UK – estimates suggest the number of EU workers on payrolls fell by 7.4% from the start of the pandemic to the end of last year, linked to workers returning to home nations during the pandemic.

Most UK data points are back to or above last summer's levels

Cost pressures are rising, but is it enough to bother the Bank of England?

Secondly, the PMIs make it pretty clear that cost pressures are rising and that firms feel comfortable with passing these onto consumers. There was limited evidence of reopening-linked price spikes in the April CPI report, though there’s little doubt that some demand/supply imbalances (amplified by global pressures) will help push inflation above target towards the end of the summer/early autumn.

The key question for the Bank of England of course is whether this persists into 2022 and beyond, and we’re inclined to say inflation will gradually trend lower from this time next year, reducing the immediate pressure on policymakers to consider rate hikes.

Global demand recovery is helping to offset Brexit disruption for manufacturers

Finally, the manufacturing sector has continued to bounce back from the Brexit-related disruption earlier in the year. New export orders were the fastest on record, which is linked to the rebound in global trade. Admittedly, this doesn’t necessarily tell us that UK trade has fully bounced back to its pre-trade deal levels. Official data shows that manufacturing-linked exports to the EU have bounced back more quickly than other products, most notably food/agriculture. And the UK’s share of the total EU’s imports is still lower than it was last year.

Expect strong second quarter growth

Overall, the UK’s growth prospects look good this year. Unless concerns surrounding the India-originating Covid variant start to reverse the recent rise in consumer/business confidence, we expect just-shy of 7% growth this year, including 5% growth in the second quarter. It’s worth noting that this latter figure is mainly a function of the April/May reopenings, and we don’t think a delay to the final lifting of restrictions in June necessarily needs to make a significant impact on near-term GDP.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more