- Quick take

UK retail sales remain solid despite May contraction

- 18 June 2021

May's decline in UK retail sales marks only a modest correction after a surge in April when shops reopened their doors. Retailers will be helped over the next few months by rising confidence and pent-up savings, though the reopening of services unsurprisingly means that retailers may not fully cash in on the consumer recovery

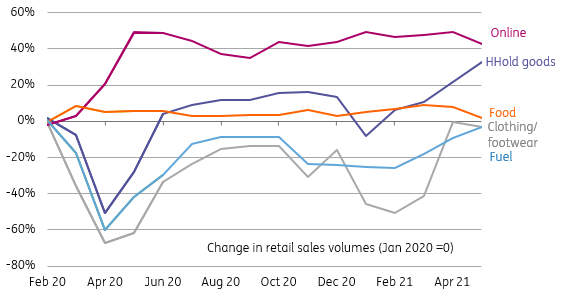

UK retail sales came in a bit lower in May following a strong April, which had been linked to the reopening of in-store shopping. Spending was down 1.4% on the month, though to put things in perspective we’re still roughly 10% above pre-virus levels. The ONS ascribes a large part of May’s moderation to a slowdown in food sales as people resumed eating out again.

UK retail sales - percentage change since Jan 2020

This latter point is, in a nutshell, the potential challenge for retailers over the next few months: maintaining the level of spending as consumers resume spending on services that have been shuttered for the past few months.

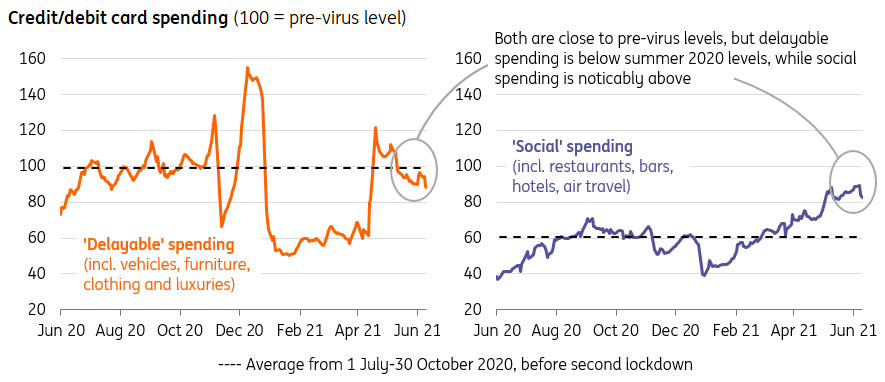

In fact there are already, unsurprisingly, some hints that this rebalancing is happening. Credit/debit card data shows social spending noticeably above last summer’s average, when restrictions were also low. Meanwhile delayable spending, which includes things like furniture and other luxury items, is tracking slightly below last summer’s levels - though admittedly the data is noisy.

The good news for retailers of course is that consumer confidence has soared as a result of the vaccine programme, and it’s clear from mobility data that people are more confident about going-out-and-about than they were after the first wave last summer. And the keen interest in returning to hospitality carries benefits for some retailers too – it’s undoubtedly a factor in the recent recovery in clothing sales, for instance.

There’s also little doubt that consumers have the resources to spend in the form of pent-up savings, albeit unlike the US, these are heavily concentrated among higher earners who are more likely to save than spend.

Consumers are increasingly switching spending to services

In other words, consumer spending is likely to help drive GDP back close to, or maybe even back to, pre-Covid levels by the end of the year. However retailers – particularly physical stores – may not feel the full benefit of the pent-up demand story as consumers pivot back to spending on services. And that suggests the period of consolidation we’ve seen among retailers over recent months may well continue, though it’s worth saying that the recent extension of the eviction ban will help here, given concerns about rent arrears in the sector.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more