- Quick take

- 22 May 2020

- United Kingdom

UK: No quick return after retail sales plunge

Consumer caution and ongoing social distancing measures pose a challenge to Britain's already fragile high street

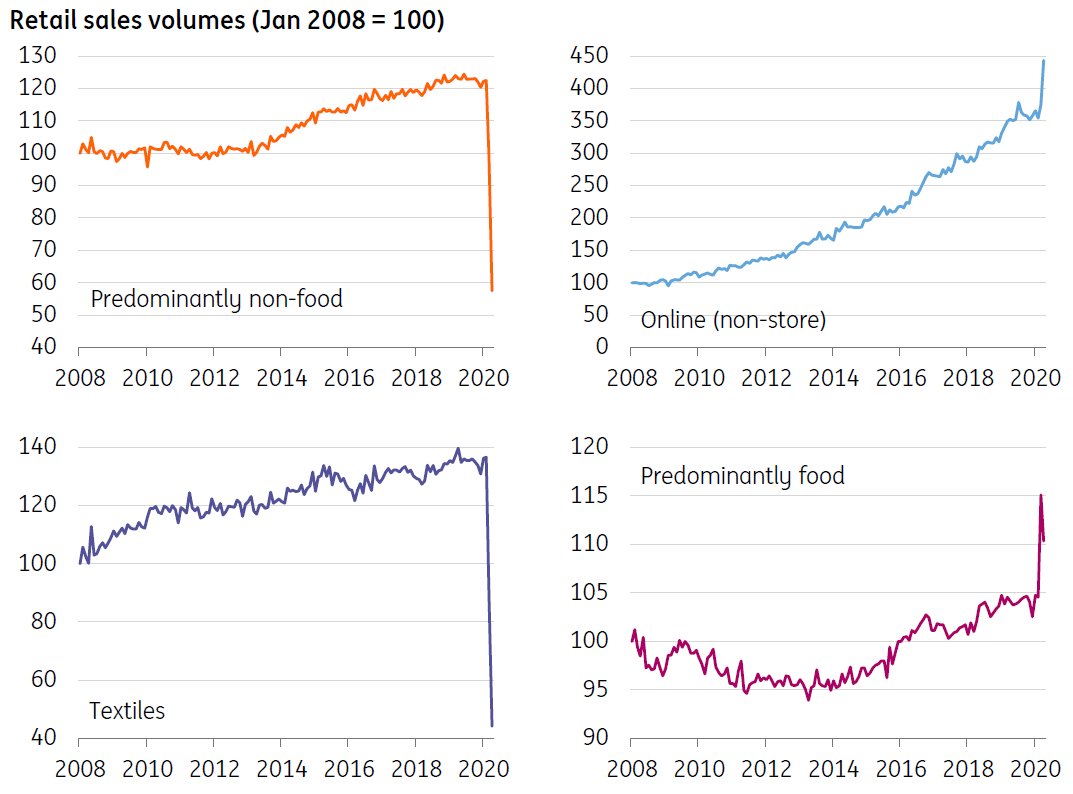

Sales plunge comes at tough time for retailers

We may be in an era where financial markets have become desensitised to big percentages, but April’s 15.2% decline in UK retail sales (ex fuel) is nevertheless shocking. It will come as no surprise that this is by far the worst monthly reading we’ve seen in the survey’s history, and in level-terms it means sales were below where they were back in 2008/9.

All of this comes at an already precarious time for the British high street. The sharp fall in the value of the pound and a prolonged period of subdued consumer confidence following the 2016 referendum had hit demand over recent years, while retailers were contending with the combined cost pressures of consecutive increases in the minimum wage, and more recently, inventory building around Brexit deadlines.

How Covid-19 has hit UK retail sales

While sales will receive a boost in June, assuming stores are able to reopen under the second phase of the government’s Covid-19 plan, the road to recovery will be tough.

Social distancing requirements will mean that for many businesses, operating profitably will remain challenging - particularly for those that are more reliant on a high volume, low margin model. And consumers appear reluctant to return to the high street even after shops are able to reopen.

Recent surveying from YouGov showed that just under half of people would be uncomfortable with returning to a clothing shop, although the jury is out on whether the public will become more relaxed by the time retailers do reopen next month.

Consumer caution likely to accelerate challenges facing high street

Over the medium-term, the turbulence in the jobs market means that consumer confidence, as well as aggregate spending power, is likely to remain heavily subdued. As we discussed earlier in the week, there are growing concerns that those sectors hardest hit by the shutdowns (including retail) could see a rise in redundancies further down line, depending on how the government’s furlough scheme evolves.

All of these factors are likely to accentuate the trend away from physical retail we’ve seen over recent years. Online spending unsurprisingly saw an 18% jump in April, taking the overall share of internet sales to 30% of the total, from 22% in March. And interestingly, the UK had already been further ahead in the shift to online spending compared to other countries, which perhaps meant it was slightly better set-up for the sharp changes of the past two months.

Still, the bulk of shopping is nevertheless done in physical retail outlets, and while the balance will be redressed to a certain extent when stores reopen, in many cases shops may not reopen at all. According to the Local Data Company, store openings have fallen consistently since 2015, while closures have risen by around 14% over that period. The vacancy rate in the retail space has crept higher over recent years, and we assume this trend will only accelerate.

Britain, breakout and Brexit

The prospect for a 'V'-shaped recovery in the UK is fading as the country still searches for a breakout from the coronavirus shutdown. And there's a more pressing matter for retailers as surveys suggest people are still scared about going back into shops even after stringent restrictions are lifted. And don't forget about Brexit. Talks don't seem to be going well with the European Union. And as ING's James Smith explains, we don't expect the British economy to return to pre-crisis levels until 2022.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more