- Quick take

- 1 August 2018

- United Kingdom

UK manufacturing output slips as Brexit risks mount

Life is unlikely to get any easier for UK manufacturers as talk of a 'no deal' Brexit continues to ramp up

At 54.0, the latest UK manufacturing PMI is the lowest in three months and is a far cry from the levels seen towards the end of 2017. Weaker domestic demand saw new orders fall and the rate of output growth slip to the lowest in 16 months. Interestingly though, demand from abroad hit a six-month high, implying that firms are still reaping the rewards of better global growth, despite the recent moderation in Europe.

But over coming months, life for manufacturers is unlikely to get any easier. The recent escalation in trade tensions is clearly a challenge, but increasingly the biggest headache for businesses is likely to be the threat of a ‘no deal’ Brexit. This scenario would likely see huge congestion at ports and disruption to supply chains. While we suspect the probability of the UK leaving without an agreement in March next year is relatively low, an agreement may not come until late in the day.

Until then, confidence could begin to fall as uncertainty increases – the latest PMI suggests the degree of positive sentiment is already at a 21-month low.

| 54.0 |

UK manufacturing PMI |

| Lower than expected | |

Having said all of that, today’s slip in the PMI is unlikely to faze Bank of England policymakers ahead of tomorrow’s decision. Representing around 10% of output, manufacturing is a relatively small part of the UK growth mix. Importantly, the recent data flow – particularly in the much larger service sector – has largely backed up the Bank’s view that the economy has regained poise after the weak first quarter.

For that reason, we think the Bank of England will increase interest rates this week. But the key thing to watch is what the Bank has to say on its next steps. In an ideal world, we think policymakers would like to hike rates again much sooner than markets are currently pricing (towards the end of 2019). But with Brexit uncertainty considerably ramping up, realistically we think the Bank will struggle to raise rates again before the UK leaves the EU next March.

After Thursday, we currently don’t anticipate another hike before May 2019.

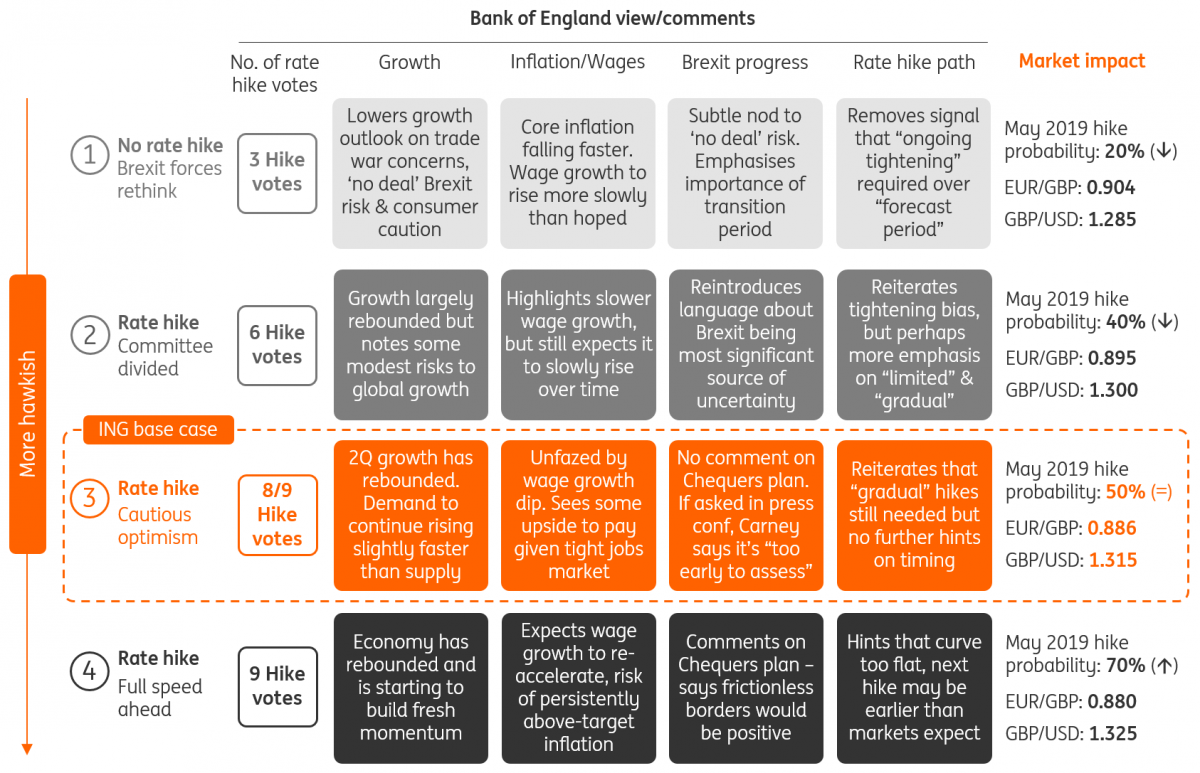

In case you missed it: Our August BoE scenarios

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more