- Quick take

- 18 May 2022

- United Kingdom

UK inflation hits 9% but it may well have peaked

While there are plenty of upside risks to UK inflation, we suspect April's 9% figure will mark the peak. Certain goods categories will start to pull down the headline rate, even if further pressure in food and services is yet to come. The key thing for the Bank of England is that inflation is likely to be below target by the end of 2023

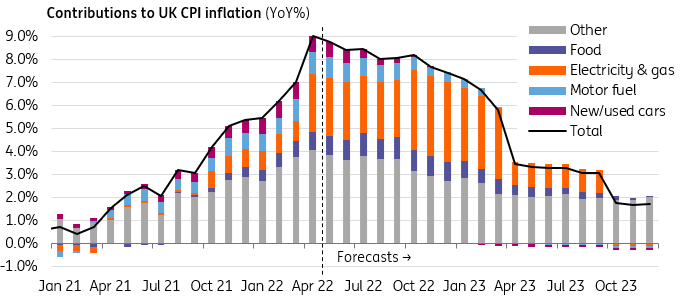

UK inflation reached 9% in April as the well-telegraphed 54% increase in the household energy cap fed through to the CPI basket. That change in electricity and gas prices, combined with the recent pressure on petrol costs, means energy is now contributing three-and-a-half percentage points to the overall inflation rate.

The key question now is whether inflation has peaked, and we think the answer is probably yes. Admittedly a lot hinges on the next energy price cap announcement in October, which we expect will deliver around a 40% increase in prices – or 30% once the government’s £200/household rebate is factored in. We don’t yet know exactly how that subsidy will be treated in the CPI figures, and while it is simply an accounting point, it might hold the key to answering whether we’ll get a second ‘twin peak’ in inflation later this year (the chart below assumes the rebate is factored in).

Energy is now contributing 3.5pp to overall inflation

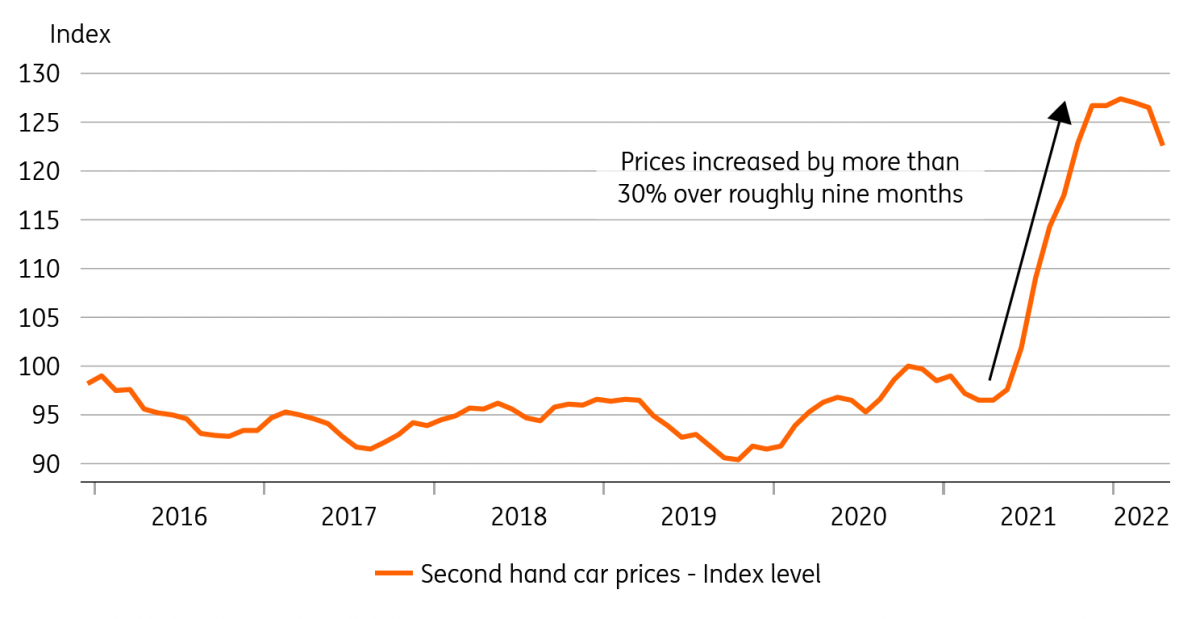

Away from energy, there’s going to be increasing downward pressure on the headline rate from certain goods prices. Like in the US, used cars are the most obvious example, and having risen by more than 30% over around nine months to January, prices fell by 3% last month. Given that the price increases really began to ramp up from last spring, we’re likely to see the likes of used cars (and other similar goods categories) contribute less and less to the overall annual inflation rate.

That said, inflation is unlikely to fall quickly. That downward pressure from certain goods categories will be offset by increases in food prices as well as services. Yesterday’s jobs numbers continued to show a tight hiring market characterised by ongoing labour supply issues, and in the short term that pressure on pay is likely to be passed onto consumers.

Used car prices have started to fall in level terms

In short, inflation is unlikely to dip much below 8% for the majority of this year. However, the headline rate will fall dramatically next April assuming we don’t get another leg higher in electricity prices and indeed CPI will probably be a little below target by the end of 2023. The Bank of England’s forecasts – or at least those based on market interest rate expectations – have shown something similar. We therefore expect another hike in June and August before the committee most likely pauses its tightening cycle.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more