- Quick take

- 12 August 2021

- United Kingdom

UK growth surges, but can it last?

The spread of the Delta variant has put the brakes on the recovery after a strong second quarter. While we're not expecting a return to significantly negative growth, the rise in Covid-19 cases suggests it may still be another couple of quarters before the economy has returned to it's pre-virus level

The latest UK GDP data confirms what we already knew – that the economy was on fire through the second quarter.

Admittedly, a large part of the 4.8% quarterly growth is a simple function of the reopenings. And indeed, if we look at June data specifically, 0.45% of the 1% monthly growth came from health, which is linked to people visiting their doctor more. Still, quirks aside, we saw a clear increase in optimism among both consumers and businesses through the spring, and that will undoubtedly have helped drive a faster recovery in activity.

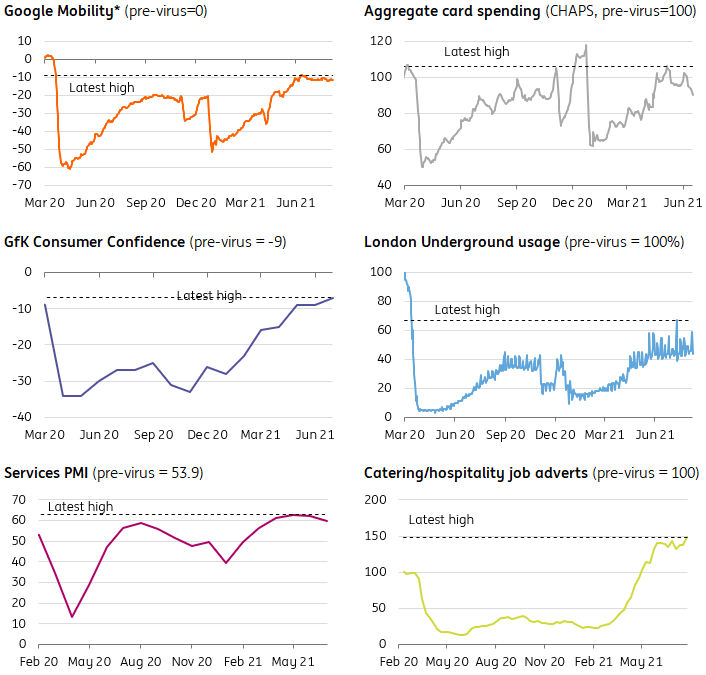

Of course, this is largely ‘old news’. The sharp rise in Covid-19 cases through July appears to have stopped the recovery in its tracks. Mobility levels – measured either by Google data or public transport usage – have plateaued, while aggregate spending has ticked slightly lower.

In practice, we think the July and August GDP readings will average at roughly 0.2-0.3%, which translates into overall third-quarter growth in the region of 1.5% - quite a bit lower than the 3% figure the Bank of England is pencilling in.

Ultimately a lot depends on how much consumer caution has crept in over recent weeks – and the news here is still fairly mixed.

Encouragingly, and despite hundreds of thousands of people having to self-isolate through July, social spending has stayed supported, bucking the overall decline in card expenditure since Covid-19 cases started rising rapidly.

And if we look at the weekly ONS survey of individuals, the proportion of people visiting indoor hospitality was actually a little higher at the start of August than it had been in previous weeks.

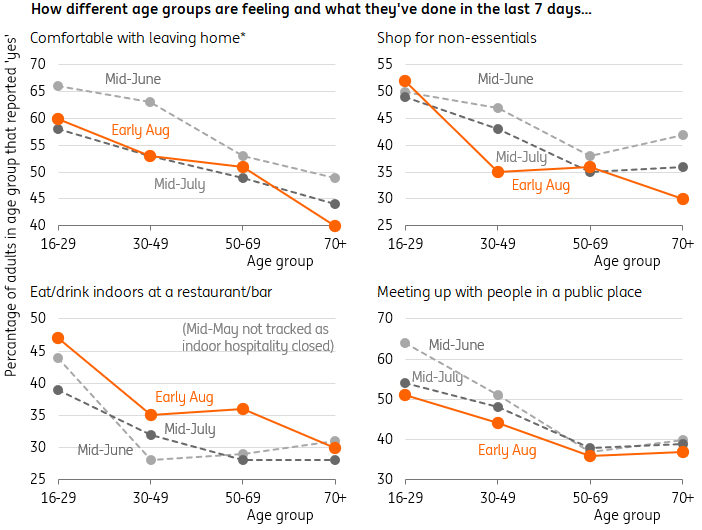

However, the same survey nevertheless shows a bit of increased nervousness about leaving home, particularly in older age groups. Even though vaccines have raised the bar to implement fresh lockdowns considerably, some of this caution will likely persist in the autumn and winter.

That suggests further gains in growth are going to be harder to achieve – and that while the economy is within 2.3% of its pre-virus level (as of June), it could still feasibly take until early next year for the remaining ground to be made up.

The latest on post-Brexit trade

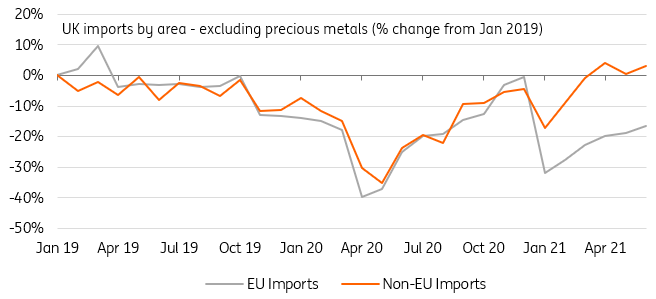

Away from GDP, one piece of good news is that UK exports to Europe have continued to recover after their turbulent start to the year - and, in fact, are now back to pre-pandemic levels once precious metals are stripped out. That suggests that businesses have largely adapted to the new processes, and a good acid test of that is that food exports are essentially back to late-2020 levels. Agriculture was arguably the sector most acutely affected by new trade rules and bureaucracy.

The major caveat here is that the UK’s official data still looks considerably better than that from Eurostat, which the ONS reckons is down to the way the latter now records the origin of shipments from Britain.

The imports side is more of a puzzle. Halfway into the year, shipments from the EU are still well down on 2020 levels – and are clearly underperforming shipments from outside the single market. Our initial sense was that this was down to firms running down stocks built up in late 2020, but that should probably have run its course.

In short, while UK trade has undoubtedly recovered from earlier this year, our sense is the UK is still struggling to fully benefit from the wider recovery in world trade over recent months.

UK imports from Europe have been slow to recover

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more