UK economic output falls further than expected in July

The monthly GDP numbers have been highly volatile, but we do expect slower growth over coming months as the cooler jobs market and higher rates continue to bite

The UK economy contracted by half a percent in July, though frankly, these numbers have been all over the place recently.

Remember that output had increased by the same percentage in June, thanks in no small part to a highly unusual surge in manufacturing. That boost to production, which was linked to car production and pharmaceuticals, partially unwound in July. But the hit from there was amplified by the service sector, which saw output fall by 0.5%. Strikes offer part of the explanation, with losses most visible in health. But we also saw declines in a range of other sectors, including IT and admin/support services, and this is harder to explain.

Cutting through the noise, the economy seems to be still growing, albeit fractionally. The change in activity over the past three months relative to the three months before is still slightly positive. We think the economy is likely to more or less flatline over coming quarters – and a mild recession can’t be ruled out.

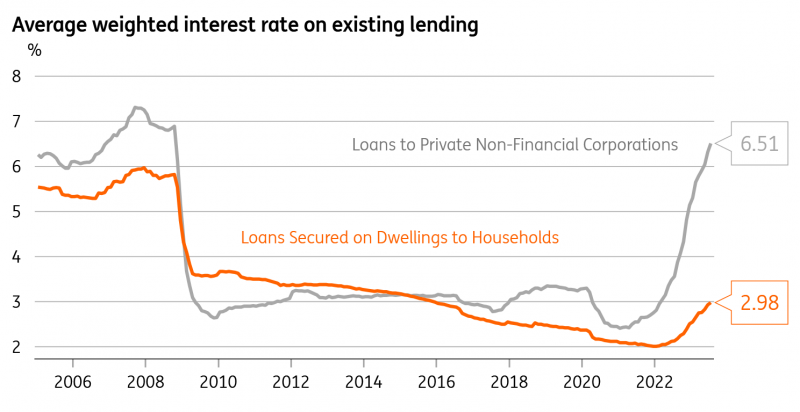

The jobs market is cooling, while the impact of higher rates is still yet to hit the economy. The average rate paid on outstanding mortgages is roughly 3%, up from a low of 2% but well below the 6%+ rates being quoted on two-year mortgages for new lending. As more and more borrowers refinance, we expect the average mortgage rate to rise above 4% in 2024, even without any further Bank of England rate hikes. That’s a gradual process so we don’t expect an abrupt hit to GDP in any specific quarter, but it will act as an ever-increasing drag on consumer spending.

Corporates have felt the impact of higher rates more quickly than households

The caveat of course is that considerably more households own their home outright than 10 years ago (39%), relative to those with a mortgage (28%). Then again, businesses have already felt the full effect of higher borrowing costs, given lending is more typically on floating rates.

Back to this latest data, and given the volatility in the GDP figures, we expect the Bank of England to largely ignore them. Officials have been clear that they are focused on wage growth, services inflation and labour market slack – and not a lot else. We expect one more rate hike at next week’s meeting, before a pause in November.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

UK GDPDownload

Download snap