- Quick take

- 5 June

- Turkey

Turkish inflation beats consensus again in May

Higher-than-expected May inflation led to a slight increase in the annual figure, driven mainly by processed food, clothing and transportation services

Monthly inflation in May was 1.7% versus the market consensus of 1.5%, while annual inflation inched up to 32.6% (vs the Central Bank of Turkey's target of 24% and forecast of 26% in the latest inflation report) from 32.4% a month ago. While this shows that the disinflation trend has not resumed yet, processed food, clothing and transportation services were the key drivers of the worse-than-expected reading.

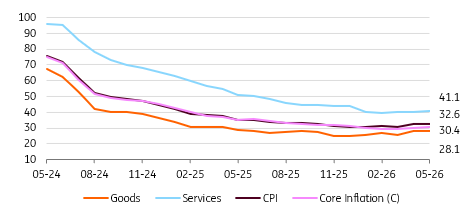

Evolution of annual inflation (%)

Core inflation (CPI-C) rose by 2.9% MoM, and maintained strength, leading to an increase in the annual rate to 30.4%, while the managed currency by the central bank, with modest nominal TRY depreciation in recent months, limited the increase. In other words, although the average increase in the USD/TRY accelerated to 1.6% in May compared to the previous month, its annual increase remaining at around 21-22% – significantly below inflation in the same period – indicates that the CBT maintains its exchange rate policy, which supports the disinflation objective through the cost channel.

In May, PPI stood at 2.8% MoM and moved up to 28.9% YoY, maintaining the uptrend since the beginning of this year. In addition to electricity, gas production and distribution, food products and plastics were the major drivers of the May PPI increase, likely reflecting the impact of the Gulf War on some industrial materials. Global commodity prices and particularly oil prices in the current geopolitical backdrop will remain the key risk factors to the PPI, which is on a gradual uptrend.

Preliminary seasonally adjusted data, set to be published by TurkStat and closely monitored by the CBT, indicate that the underlying inflation trend in three-month moving average terms recorded an improvement last month, though remaining well above the levels realised at end-2025, implying challenges to the disinflation in the current environment.

Breakdown of the data shows that:

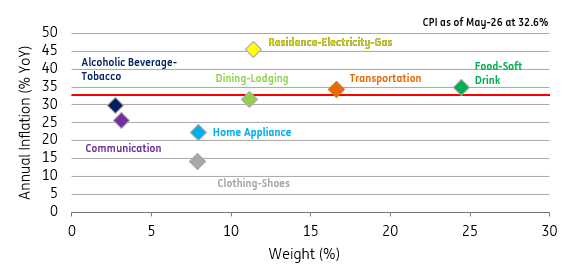

- The clothing group made the largest contribution to the headline (0.75ppt), driven by seasonality, though recording a higher increase than the long-term May average in the current series, attributable to normalisation of prices in this group. Whether the increase in annual inflation from 6-7% range in recent months to 13.6% in May continues will be important for price developments in the near term.

- The transportation group was another contributor (0.90ppt) on the back of transportation services, while the drop in diesel limited the pace in this group.

- The housing group followed (0.27ppt) with the carryover effect from administrative price adjustments a month ago. Rents, which play an important role in persisting services pricing pressures, on the other hand, continued to moderate to 49.8%.

- The food group dragged the headline (-0.12ppt) thanks to a pronounced 4% drop in unprocessed food prices driven by fresh fruits and vegetables. However, processed food showed a strong increase, limiting the supportive impact of the unprocessed side. Accordingly, annual inflation inched up to 34.9% vs the CBT’s assumption for this item at 26.3% for this year.

As a result:

- Goods inflation fell slightly to 28.1% YoY, while core goods inflation moved up to 17.3%, though remaining subdued given the CBT’s tight grip on the exchange rate supporting disinflation in this group.

- Services inflation has remained elevated at 41.1% YoY, showing the extent of inertia and recent pressure in transportation services.

Annual inflation in expenditure groups

Overall, May inflation has not yet signalled a return to the disinflation trend, confirming that the path ahead remains challenging. Uncertainty surrounding oil prices – along with their spillover effects on other commodity prices – continues to pose risks to the inflation outlook, despite the government’s decision to cushion part of the oil price shock by adjusting taxes on gasoline. Food inflation also contributes to this uncertainty, as it remains exposed to risks in both directions, shaped by the anticipated increase in agricultural production and potential pressures stemming from fertiliser costs.

Against this backdrop, we expect the central bank to keep interest rates unchanged at the June MPC meeting, taking into account recent macroprudential tightening with reduced caps on lending growth. Nevertheless, ongoing geopolitical uncertainties and domestic political developments may call for a more cautious approach, which could lead to an upward adjustment in the policy rate – from 37% to the current effective funding rate of around 40%.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more