- Quick take

Turkish current account deficit widens further

- 11 April 2018

- Turkey

The current account balance recorded a deficit of USD 4.2bn, while the 12-month rolling deficit kept widening on the back of resilient domestic demand, continuing gold imports and a rising energy bill

Current account balance that has been on a widening trend since early 2017 recorded a deficit of USD 4.2bn in February, aligned with market consensus and our call. The latest figure pulled the 12-month rolling deficit up to USD 53.3bn, which is the highest since April 2014.

The deterioration in the monthly deficit versus the same period in 2017 is mainly attributable to the ongoing expansion in the trade deficit with accelerating imports on the back of rising gold and energy as well as the continuous uptrend in core imports.

As a positive note, the pace of the deterioration in core balance slowed down in February. Services income has maintained improvement on the back of a sharp recovery in net tourism revenues by 47% YoY, while the contraction in primary income deficit offset a decline in secondary income surplus.

External balances (USD bn)

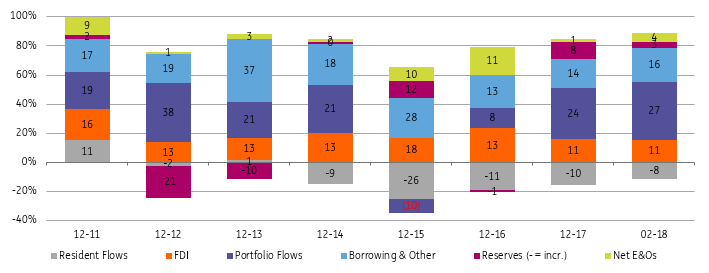

On the financing front, capital flow outlook has weakened with USD 2.5bn, standing below the monthly current account deficit, after strong portfolio inflows in January driven by debt-creating inflows. Official reserves recorded USD0.3bn decline, despite the positive impact of net errors and omissions with USD1.4bn.

In the breakdown of the capital account, borrowing of corporates by USD1.9bn (USD1.7bn of which in long-term) and banks by USD0.6bn long-term borrowing stood out as the major flow item. The long-term debt rollover ratios were 146% and 320% for banks and corporates, respectively. Portfolio inflows turned out to be weaker as banks’ USD0.5bn bond issuance was offset by non-residents’ sales in bond and equity markets. Foreign direct investment has remained weak.

Breakdown of current account financing (USD bn)

Overall, strength in robust domestic demand, higher energy prices and unexpectedly strong gold imports push the current account deficit wider in recent months.

This renders the currency vulnerable to sudden shifts in investor sentiment along with the continuation of inflationary pressures. Capital flow outlook that deteriorated last year with increasing reliance on portfolio flows and short-term funding will remain in the spotlight this year, leaving little room for policy complacency.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more