- Quick take

- 11 December 2017

- Turkey

Turkish current account deficit widens further in October

October current account deficit came in better than market consensus but we expect it to lose momentum next year due to moderating growth and softening energy prices

Breakdown of C/A Balance (USD bn)

The current account deficit in October stood at USD3.8bn and was better than market consensus at USD4.1bn and our call at USD3.9bn, pulling the 12-month rolling deficit up to USD41.9bn, the highest since mid-2015.

The breakdown shows the deterioration versus the same month in 2016, is mainly attributable to expansion in the trade deficit with higher oil prices and weakening net gold trade while strength in domestic demand has also contributed with widening the core deficit in the second half of this year. Primary income that is in negative territory in general, declined further with profit transfers abroad.

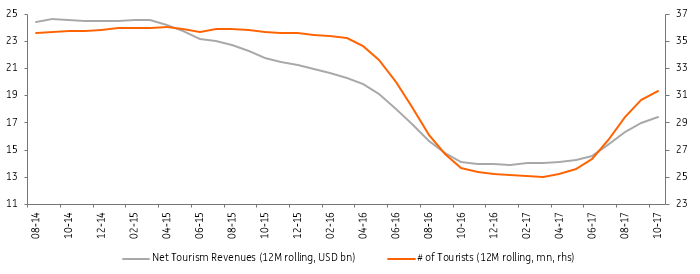

On the flipside, services income has remained on a recovery path, thanks to the jump in net tourism revenues by around 30% YoY with Russian and MENA tourists.

Tourism revenues

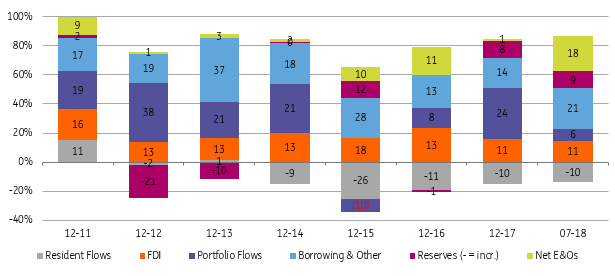

On the financing front, despite volatility in local financial markets following visa spat between the US and Turkey, October saw strength in inflows, standing at USD5.0bn. Official reserves recorded USD5.0bn increase also with the contribution of USD3.8bn net errors and omissions, showing acceleration again from May onwards.

In the breakdown of the capital account, rising borrowing by banks and corporates was the main reason for improving flow outlook. In October, corporates borrowed a net USD1.6bn, while the banking sector was a net borrower with USD2.4bn (USD1.3bn of which in long-term). Accordingly, the long-term (LT) rollover ratio for the corporate sector improved marginally to 109% on an annual basis, up for the first time since Jul-16. The banking sector’s 12-month long-term debt rollover ratio, on the other hand, stood at 95% in October, recording increase in two months in a row. On the flip side, foreigners’ purchases in domestic bond and equity markets that were strong in previous months have lost significant momentum.

Other items that supported flow outlook were 1) banks’ bond issuance amounting to USD0.9bn, 2) corporates issuance at USD0.7bn 3) Trade credits amounting to USD0.8bn. Inward FDI, on the other hand, stood at USD0.7bn, somewhat below of the monthly average in recent years. On the flip side, a rise in locals' assets held abroad of USD2.2bn mainly via deposits was also noteworthy.

Financing breakdown (12M rolling basis, USD bn)

Overall, the 12-month rolling current account deficit has followed a fluctuating uptrend since the beginning of this year mainly attributable to widening trade deficit with gold and oil trade while core trade has also shown signals of deterioration in the last few months on the back of robust domestic demand.

In the remainder of the year, we expect the external deficit to gradually increase, though likely to lose momentum next year with moderating growth as well as expected softening in energy prices.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more