- Quick take

Turkish Central Bank to stay on hold

- 18 April 2019

- Turkey

We expect the Central Bank of Turkey to keep its one-week repo rate on hold at 24% and continue to be cautious in signalling rate cuts

In its rate setting meeting on 25 April, we expect the CBT to keep its one-week repo rate steady at 24% amid macro uncertainties and recent currency volatility. We think the bank will remain cautious in signalling any rate cuts and in fact, we do not rule out more hawkish messages in its accompanying statement. The CBT will likely maintain a tight stance in the post-election period and avoid any premature policy rate adjustment to maintain price stability and support financial stability.

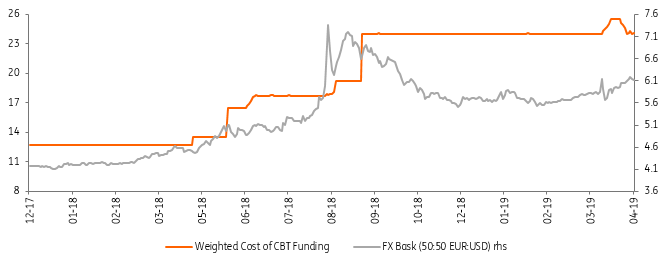

Cost of CBT Funding vs TRY

Last month, concerns about financial stability increased on the back of:

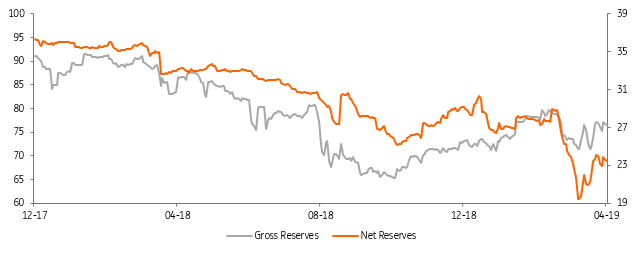

- A drop in FX reserves. Net foreign assets of the CBT (difference between FX assets that track gross reserves including gold and FX liabilities) dropped from US$28.9 billion in early March to US$19.4 billion on 22 March, despite a relatively small external deficit and the Treasury’s significant borrowing of US$6.4 billion this year.

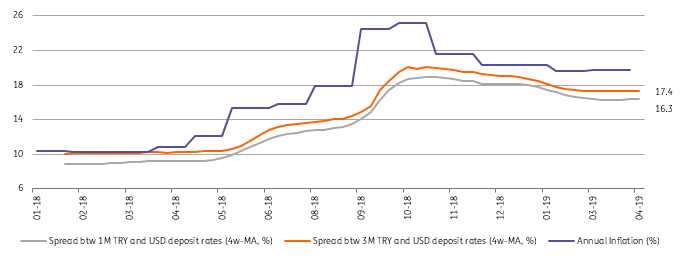

- Evidence of a further increase in residents' FX deposit holdings. Given elevated inflation and low real return in TL investments (i.e. TL deposits), residents have increased their FX deposits by US$30 billion since September, mostly driven by households. This takes the share of FX deposits to 54% of the total as of the beginning of April.

The CBT tightened its liquidity policy by suspending funding of the banking sector through the one-week repo rate (at 24.0%) and directing efforts to the ON lending (at 25.5%) with a 150 basis point adjustment in the effective cost of funding.

CBT Reserves (US$ bn)

To support FX reserves, the CBT also cancelled FX deposits against TL deposit auctions and increased banks’ transaction limits in the swap market to 40% of their pre-determined FX market transaction limits from 10%, in three separate moves. Accordingly, the CBT’s net FX reserves have improved to US$23.5 billion as of 15 April, reflecting the impact of these measures on FX assets.

Following a normalisation in financial markets, the CBT started one-week repo auctions again on 8 April, readjusting the effective cost of funding to 24%. But the bank continues to monitor the performance of the lira as any sharp currency weakening and consequent FX pass-through would pose significant upside risks to the inflation outlook. As of March, annual inflation was flat while core inflation continued to decelerate. In the period ahead, exchange rate developments will be key, though the current economic backdrop, with ongoing weakness in domestic demand and base effects, will remain supportive. We should not rule out the likely impact from a marked deterioration in pricing behaviour and inflation expectations.

Interest Rate Differential btw FX and TRY Deposits

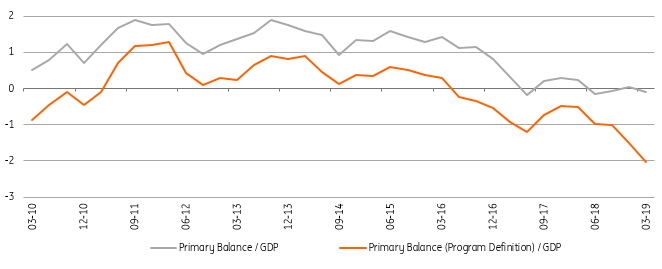

On the fiscal front, the budget performance has shown a deterioration in the first quarter due to continuing weakness in tax generation and strong growth in primary expenditures. Weak economic activity and spending pressures, along with the ongoing uptrend in interest expenditures, pull the 12-month rolling budget deficit above the target set for 2019 in the New Economy Program.

The reform package announced by Finance Minister Berat Albayrak focuses on maintaining fiscal discipline. It reiterates the government’s commitment to budgetary discipline and pledges reforms in key areas like taxation, social security, unregistered economy etc. The package also focuses on boosting savings, strengthening the financial sector and facilitating disinflation. Implementing all of this successfully will be instrumental to improving confidence and delivering reductions in risk premia and long-term interest rates.

Central Administration Budget Primary Balance (%)

Against this backdrop, we don’t look for a policy rate change in the April MPC and do not expect a rate cut in the first half of the year. Depending on the performance of the lira, a moderate monetary easing may be on the agenda in the second half, likely in the last quarter.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more