- Quick take

Turkish Central Bank: Ready to deliver more rate cuts

- 6 September 2019

- Turkey

We expect the CBT to cut its policy rate by 175bp to 18% for the next MPC meeting on September 12 on the back of a faster than expected recovery in the inflation outlook and ongoing improvement trends in inflation expectations. The continuation of the easing cycle is also supported by improving external financial conditions

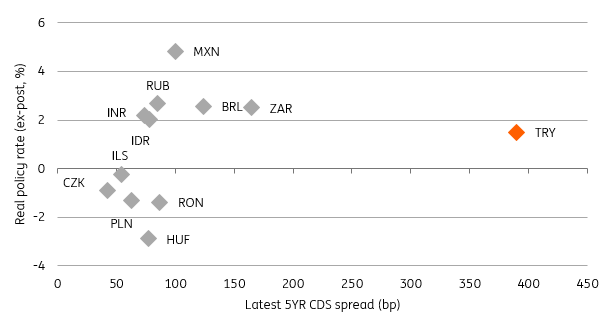

After a deeper than expected easing in July, we expect the CBT to deliver another policy rate cut of 175bp, to 18%, at the next MPC meeting on September 12 on the back of a faster than expected recovery in the inflation outlook and ongoing improvement trends in inflation expectations. The continuation of the easing cycle is also supported by improving external financial conditions. This will bring the real policy rate on which the CBT bases its decisions, rather than the nominal rate, to 300bp. That's the latest average of major emerging market peers (namely Mexico, Brazil, Russia and South Africa). The risks to our call remain tilted to the upside.

Inflation expectations (%)

Governor Uysal’s early remark that “the design of monetary policy will be based on a data-focused approach that takes into account all macroeconomic indicators, primarily inflation and economic activity” provides guidance that not only inflation but activity matters for the policy implementation. Accordingly, the CBT linked required reserve ratios (RRRs) and remunerations to credit growth, given private banks’ hesitancy to expand lending.

The CBT’s macro prudential tool to incentivise lending is based on TL loan growth (not the FX part) and comes with a cap of 20% (beyond this level there's no preferential treatment for banks). Currently, banks differentiate in their lending appetite with state banks being above of the lower threshold (10%) already eligible for the CBT’s reserve requirement tool while private banks are generally standing behind. In fact, annual TL loan growth in the sector (as of 29 Aug) is +0.2% (15.7% in state banks and -8.6% in non-state banks), while FX growth in USD terms is -5.4% (state: -3.1%, non-state: -6.3%). So, the behavioural difference is mainly on TL lending and the adjustments may support credit growth.

Given the current state of domestic demand, despite the improvements in private consumption in 2Q, this macro-prudential measure of the CBT should not weigh on the inflation outlook in the short term. In fact, inflation surprised to the downside for the fifth consecutive month in August thanks to still weak domestic demand, relative strength in TRY, gradually improving inflation expectations, a plunge in unprocessed food prices and downward pressure on energy prices, despite one-off factors such as tax and administrative price adjustments.

Annual core inflation also improved to the lowest level since May-18, showing easing price pressures. As an indicator for underlying price dynamics, the diffusion index has remained below trend. Inflation will drop very rapidly in September and reverse thereafter because of large base effects, still leaving room for the continuation of the easing cycle by the CBT.

Despite current aggressive market pricing of more than a 400bp cut by the Monetary Policy Committee, the CBT should be cautious given that inflation expectations are still not well anchored and the high inertia we see, notably with services' inflation. Global economic uncertainty and the impact of trade tensions on potential growth remain a concern, despite the projected easing in those financial conditions.

Global political risks and still high-risk premia should be incentives for the CBT to keep the real policy rate at a 'reasonable level'. A reason for maintaining the attractiveness of TRY assets, not only for foreign investors but also residents, is the ongoing dollarisation trend in recent years, pulling the share of FX deposits in the total deposit stock to the highest level since the financial crisis in 2001.

Real Policy Rate vs CDS premium (%)

Overall, the CBT signals in the July inflation report were to maintain the ongoing disinflation process that will help reduce sovereign risk, lower long-term interest rates, and support a stronger economic recovery. This approach should lead to a relatively measured move in the September MPC compared with a deep cut in July so as to maintain a reasonable real rate to cushion local and global uncertainties. Therefore, we expect 175bp cut this month and another 100bp in October. However, we wouldn't rule out the possibility of a larger cut in September given the current relatively better risk environment and being done with easing until the year-end.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more