- Quick take

Turkish Central Bank front-loads with big rate cut

- 25 July 2019

- Turkey

Turkey’s central bank cuts its policy rate by 425bp to 19.75%. It clearly feels more confident about the strength of the ongoing disinflation trend and front-loaded the easing cycle amid an improvement in the political and geopolitical backdrop

| -425bp |

CBT policy rate changeTo 19.75% |

| Higher than expected | |

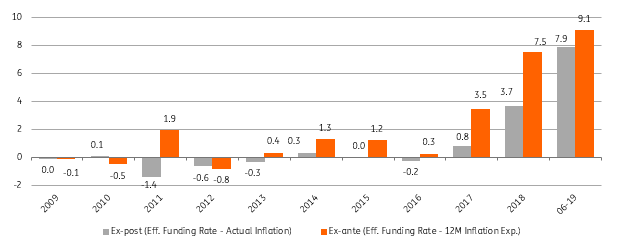

The Central Bank of Turkey (CBT) announces a deeper than expected policy easing by cutting the policy rate (1-week repo rate) by 425bp to 19.75% vs market consensus of 250bp (and our call of 200bp) at its July rate-setting meeting. With the decision, the ex-post real policy rate that had been low or sometimes even negative since the global crisis dropped sharply to 400bp from more than 800bp before vs the average ex-post policy rate for EM peers around 300-400bp.

Ahead of the MPC, there were two relevant questions, namely the extent of easing in July and guidance for the policy implementation in the period ahead. As already signalled by new Governor Murat Uysal in an interview last week, the CBT utilised “room for manoeuvre in monetary policy” and came up with a frontloaded 425bp easing by “considering all the factors affecting inflation outlook”.

In its much longer MPC statement comparing the previous months, the CBT elaborates on the recently released data and provides expectations for the near term. On the inflation front, it acknowledges the ongoing downtrend on the back of “a deceleration in unprocessed food and energy prices”, along with a contribution from “domestic demand and the tight monetary policy”. The bank will announce its inflation report next week, but in the statement, it gives evidence for the inflation forecast, stating that “inflation is likely to materialise slightly below the projections of the April Inflation Report by the end of the year”.

Central Bank Funding

As for monetary policy, the CBT reiterates its key sentence in a different form, that “keeping the disinflation process on track with the targeted path requires the continuation of a cautious monetary stance”, given the close relation between disinflation and “achieving lower sovereign risk, lower long-term interest rates, and stronger economic recovery”.So as to keep inflation on the downward path, the bank wows that “the extent of the monetary tightness will be determined by considering the indicators of the underlying inflation trend”.

In this month's statement, the CBT mentions not only its price stability objective but also its financial stability objective, likely a signal that it will continue to watch the dollarisation that has been more visible this year along with exchange rate developments.

The rest of the statement makes these points:

- The CBT envisages a relatively better growth outlook, noting a moderate recovery in economic activity with increasing competitiveness while the current account balance is expected to maintain the narrowing trend. The bank also sees a continuation of the recovery process with the support of disinflation and an improvement in financial conditions.

- It states the increasingly supportive stance of global central banks. Despite a better global backdrop for emerging market assets, the bank recognises the likely risks on capital flow outlook from higher protectionism and global economic policy uncertainties.

Overall, given the surprisingly positive inflation releases, the CBT felt more confident about the strength of the ongoing disinflation trend and frontloaded the easing cycle given the improvement in the political and geopolitical backdrop. For the rest of 2019, the base effects will facilitate a rapid decline in inflation until November and we will likely see an increase in the last two months. Given the emphasis on the disinflation process and a cautious monetary stance, the CBT will likely come up with measured moves in the upcoming MPCs as the real policy rate now is less divergent from that of other EM counterparts in line with the Governor’s objective of “a reasonable rate of real return”.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: Worse and worse

- This bundle contains 10 Articles