- Quick take

- 11 January 2023

- Turkey

Turkey posts better-than-expected current account deficit

While the current account deficit remained on an expansionary path in November, the latest data shows some loss of momentum in the pace of widening with a better-than-expected monthly reading

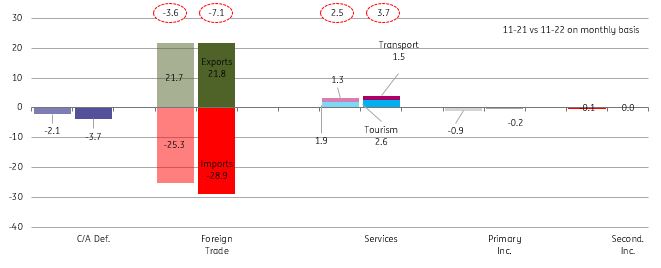

Breakdown of current account (monthly, US$bn)

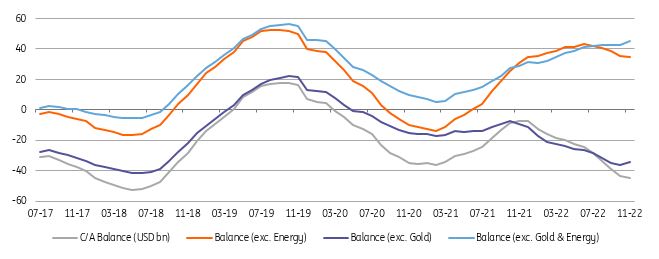

With another better-than-expected current account deficit of US$-3.7bn, the 12-month rolling deficit continued to widen although less than expected, amounting to US$45.0bn (translating into c. 5.2% of GDP) in November. The key drivers of the monthly reading over the same month of the previous year have remained the same: i) a higher energy trade deficit (US$-6.5bn vs US$-5.7bn last year) and ii) a rapid increase in net gold trade (US$-2.4bn vs US$0.6bn surplus last year). Services income, on the other hand, remained strong with a more than 46% year-on-year increase, contributing to the lower-than-expected monthly deficit. The surplus in core trade (excluding gold and energy) slightly increased and limited the deterioration in the current account.

Current account (12M rolling, $bn)

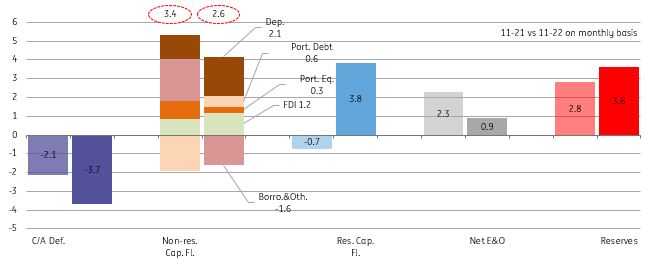

The capital account in November turned out to be positive at US$6.4bn, driven by both asset disposals by locals abroad and foreign investor inflows. With the current account deficit and continuing strength in net errors & omissions at US$0.9bn (US$22.3bn on a year-to-date basis), official reserves recorded a US$3.6bn increase.

In the breakdown of monthly flows, residents’ assets abroad recorded a US$3.8bn fall driven solely by the decline in locals’ external deposits, particularly those of banks. For the non-residents, we saw US$2.6bn of inflows: i) regarding non-debt creating flows of foreign investors, gross FDI (US$1.4bn) and purchases in the equity market (US$0.3bn) were the key items ii) for debt creating items, we observed US$0.8bn of inflows driven by non-residents’ deposits at local banks (US$2.1bn) and the Treasury’s US$1.5bn Eurobond issuance. Net borrowing, on the other hand, turned out to be negative at US$-1.8bn mainly due to the banking sector’s long-term debt repayments. Accordingly, we saw a strong long-term debt rollover rate for corporates at 94% (189% on a 12M rolling basis), while the same ratio for banks stood at 69% (82% on a 12M rolling basis).

Breakdown of financing (monthly, $bn)

We expect the deficit to top out in the coming few months. However, it will likely remain high in the near term given the marked deterioration in the terms of trade, an accommodative policy stance and weakening global growth outlook. On the capital account, we saw the impact of locals’ deposits flowing back to the country in the last two months and continued strength in net errors and omissions, which is not a stable source of funding, both leading to an increase in official reserves on a year-to-date basis. Another boost to reserves in the near term is likely if Turkey and Saudi Arabia finalise the US$5bn deposit deal.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more