- Quick take

- 22 September 2020

- Turkey

Turkey: Flat policy rate, wider corridor expected

Citing Covid-19-related uncertainty, the Central Bank of Turkey has relied on liquidity measures to tighten its stance rather than a direct rate hike. At the September MPC, we see the possibility of a wider corridor with at least a 75bp increase in the overnight lending rate and late liquidity window rate, given financial and price stability concerns

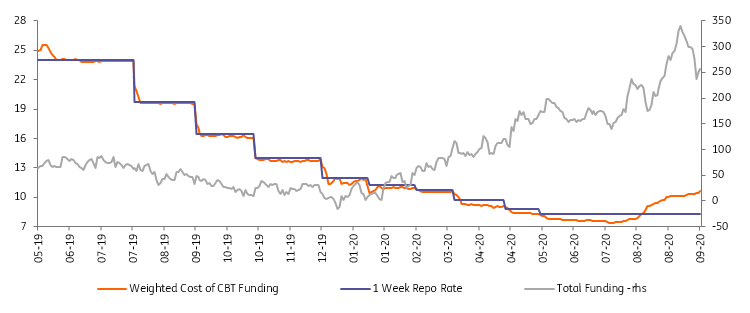

CBT Funding (Rates in %, Funding in TRY billion)

The CBT has raised its effective cost of funding rate with FX moves since early August, while it has kept the policy rate (1-week repo rate) unchanged at 8.25%. At the 24 September MPC, the bank will likely continue tightening with liquidity measures and could make an adjustment in the corridor scheme, including hiking the overnight lending rate and late liquidity window rates by 75 basis points or more to gain room to manoeuvre in the current setup towards at least 10.5% and 12.0%, respectively.

Given elevated inflation, weak capital flows, residents’ FX demand, and still high credit growth, there have been some moves by the CBT and Banking Regulation and Supervision Authority towards normalisation in recent months from the supportive policies being implemented since the breakout of pandemic. Accordingly, following the finalisation of the long rate cut cycle in June, the CBT made adjustments in the reserve requirement framework and started tightening via a change in the funding composition by hiking the effective cost of funding by more than 300bp, to 10.6% currently.

On the inflation front, exchange rate developments and elevated services inflation being highly sticky at current levels point to continuing challenges for disinflation, despite the supportive impact of weak domestic demand. The annual figure has remained elevated at 11.8% in August, while inflation expectations continued on an upward path, with 12M and 24M expectations standing at 10.15% and 8.86%, respectively, as of September. The effective cost of funding, on the other hand, in comparison to the actual cost and inflation remains low, contributing to pressure on the exchange rate and supporting the need for further tightening.

Citing Covid-19 related uncertainty, the CBT has relied on liquidity measures to tighten its stance rather than a direct policy rate hike. In the current setup, the CBT has been using newly introduced 1-month repo auctions (the interest rate being determined by liquidity conditions, and floated in 11.0-11.3% range in the last two weeks) along with the upper band of the rate corridor (at 9.75%) and late liquidity window (at 11.25%) to provide liquidity to the banking system. This allows the CBT to push the effective cost of funding up to the late liquidity window rate, implying relatively small room from the current level. Accordingly, we see the possibility of a wider corridor with at least a 75bp upward adjustment in the overnight lending rate and late liquidity window rate given continuing financial and price stability concerns, while the bank will likely keep the policy rate flat again.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more