- Quick take

- 24 July 2018

- Turkey

Turkey defies rate expectations as growth outlook dims

At the MPC meeting today, the Central Bank of Turkey kept its one-week policy rate unchanged at 17.75%, defying expectations for a 100-125 basis point rate hike. The pace of deterioration in the growth outlook, already-elevated lending rates and a belief that fiscal policy will provide support are likely reasons for this outcome

| 17.75% |

Policy rate(No change vs 100-125bp hike expectations) |

At the July rate-setting meeting, the CBT kept the one-week repo rate, the prevailing policy rate after the final simplification step at the end of May, unchanged at 17.75%. After a bigger-than-expected move in June, the CBT under-delivered this time, as the market was pricing nearly 65p of hikes for today and 125bp in total by year-end, while the consensus assumed a 100-125bp rate hike. Markets have reacted negatively to the move. Prior to the decision, the Turkish lira was around 4.75 against the US dollar but it spiked following the announcement and briefly exceeded 4.90. It's currently floating around 4.87.

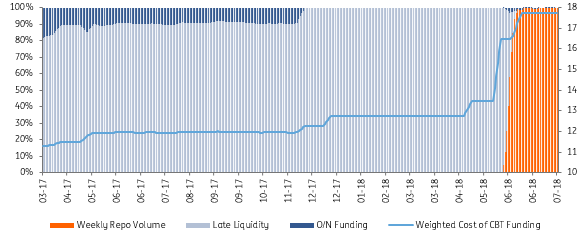

Funding Comp. & Cost of Funding (5d-MA, %)

Ahead of the meeting, we were expecting a 100 basis point hike given uncertainty about the direction of economic policy under the new management team and the sharp rise in price pressures. In its inflation assessment note released in early July, the CBT pointed to “an apparent deterioration” in the underlying trend of core inflation. June inflation clearly showed a worsening in price dynamics. The sharp deterioration in the outlook is not just confined to food prices. In fact, there's been an across-the-board deterioration in goods inflation, with annual inflation at the highest since the inception of the 2003=100 series.

Sticky services inflation also accelerated on annual basis, with rates rising to double-digit levels for the first time since the global crisis. And inflation expectations are increasingly unanchored from the CBT’s 5% target. Expectations over the next 12 and 24 months have trended upwards in recent years to an all-time high, with the former hitting 11.07% and the latter at 9.54% and continuing to rise further. In fact, in the MPC statement, the CBT reiterated “cost factors and volatility in food prices” as the drivers of inflation with “a generalised pattern” of price increases and “elevated levels of inflation and inflation expectations” as risk factors to pricing behaviour. Accordingly, the CBT vowed to keep a tight stance “for an extended period”- a new addition to the statement.

Regarding its main policy guidance, the CBT also made some revisions. While highlighting the determination to tighten further, if needed, the bank will continue to monitor 1) the lagged impact of recent monetary policy decisions and 2) the contribution of fiscal policy to the rebalancing process in addition to “inflation expectations, pricing behaviour and other factors affecting inflation” mentioned in the previous month’s statement. This suggests the CBT is reliant on an adjustment in fiscal policy to support its disinflation efforts (as recently mentioned by policymakers) and is comfortable with the current level of rates to safeguard price stability.

The CBT opted to remain silent this month likely because of the softening growth outlook. This is due to the impact of the lira's depreciation on corporate balance sheets and the repercussions for investment demand as well as the impact on credit demand from higher borrowing costs (loan rates are close to, or higher than the levels seen during the global financial crisis with the exception of mortgages). In fact, the assessment of growth by the CBT is now less positive with “a more significant” rebalancing trend and “more visible” signs of deceleration in domestic demand.

All in all, the CBT has ended its tightening cycle, in place since April, this month despite a sharp deterioration in the inflation outlook, the uptrend in forward-looking expectations and external imbalances, which leave the currency vulnerable to shifts in global risk appetite. The decision by the MPC is likely attributable to the pace of deterioration in the growth outlook, already-elevated lending rates and a belief that fiscal policy will provide support, though this would not help alleviate concerns about macro policy priorities under the new Executive Presidential system.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more