Turkey’s current account remains benign in September

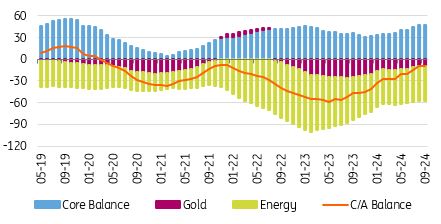

Turkey’s current account recorded another surplus in September, while its 12-month rolling deficit dropped to single digits at US$9.7bn. We think that the current policy mix is contributing to the country’s external adjustment process

September's current account balance in Turkey posted a US$3.0bn surplus, broadly in line with expectations, and was slightly better than the level we saw in the same month last year. Accordingly, the 12-month rolling deficit has maintained its narrowing trend to US$9.7bn (translating into around 0.7% of GDP) from US$9.8bn a month ago. This was its lowest reading since the end of 2021. It should also be noted that the Central Bank of Turkey also revised the cumulative current account deficit downwards in the first eight months by US$1.4bn.

Current account (12M rolling, US$bn)

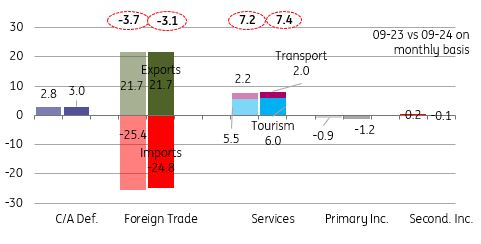

In the breakdown and compared with the same month of last year, we see: a) the gold deficit inching up to US$-0.8bn vs US$-0.7bn last year b) a slight drop in the (net) energy bill to US$3.7bn, c) a flat core trade balance at a US$1.6bn surplus, d) slightly higher services income (including tourism revenues) at US$7.4bn, e) a deterioration in primary and secondary income to US$-1.2bn and US$-0.1bn respectively. The cumulative impact of these developments was a US$0.2bn improvement in the headline current account balance in September alone.

Breakdown of current account (monthly, US$bn)

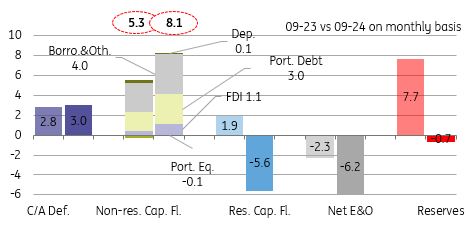

After outflows in August and for the first time since January, Turkey's capital account turned positive at US$2.5bn, while unidentified outflows remained strong at US$6.2bn. Despite the strong monthly c/a surplus and positive capital account, official reserves posted a US$0.7bn drop in September, with a large negative reading in net errors and omissions.

In the breakdown of the monthly data, residents’ movements – including outward FDI, financial assets held abroad etc. – posted US$5.6bn in outflows. On the other hand, the negative reading seen in August for non-residents turned positive at US$8.1 bn. Renewed strength in foreign flows is attributable to: a) banks’ US$1.9bn Eurobond issuances b) continuing domestic debt purchases at US$1.7bn, and c) US$5.3bn net borrowing, driven both by banks (more on a short term basis) and corporates. Rollover rates stood at 210% for corporates and 133% for banking (vs 112% and 141% respectively on a 12M rolling basis).

Breakdown of financing (monthly, US$bn)

In the first nine months of 2024, non-resident inflows improved in comparison to the same period of 2023, at US$51.8bn from US$44.3b. Meanwhile, increasing asset acquisitions of locals abroad led a decline in net identified flows to US$22bn from US$33.6bn last year. Additionally, outflows via net errors and omissions jumped to US$20.7bn vs US$8.3bn in 2023. So despite a strong recovery in Turkey's current account balance from US$-36.1bn to a mere US$-5.3bn, official reserves recorded a US$4.1bn contraction vs US$11.0bn decline last year.

Overall, Balance of Payment (BoP) dynamics have improved significantly this year. This is largely thanks to resilient exports and recovering global activity (especially in the first half, despite significant real Turkish lira appreciation), as well as contracting imports driven by a lower gold and energy deficit – though the impact of monetary policy tightening on consumption goods imports has remained limited so far. The provisional customs data released by the Ministry of Trade reveals that the foreign trade deficit recorded another drop in October by more than 10% year-on-year. This data suggests that the recovery in the external imbalances will likely continue, while the impact of the CBT's actions on the balancing of demand factors should be supportive for the current account in the near term.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap