Hungarian inflation sees a slight increase

While Hungary’s inflation accelerated in October, it caused a significant downside surprise. Services prices fell at a historical rate on a monthly basis, a one-off phenomenon. Despite the seemingly benign picture, it is FX instability rather than inflation data that will drive monetary policy decisions moving forward

| 3.2% |

Headline inflation (YoY)ING estimate 3.6% / Previous 3.0% |

| Lower than expected | |

Low base slightly accelerated inflation

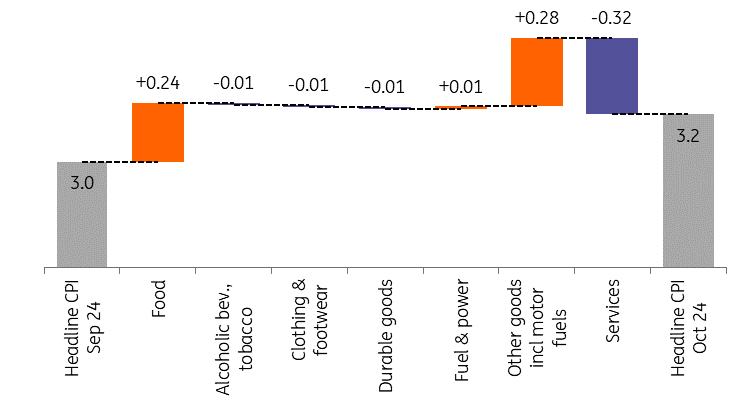

Hungarian inflation picked up slightly in October, but this was well below expectations. The latest data therefore surprised to the downside relative to market consensus. Year-on-year inflation rose from 3.0% to 3.2%, with the modest acceleration owing to a combination of a low monthly increase in the average price level of just 0.1% and a low base from a year ago.

Main drivers of the change in headline CPI (%)

The details

- The most striking (and essentially unpredictable) price developments were in telecommunications services. Here, the month-on-month fall was almost 7%, which alone subtracted 0.2 percentage points from the one-month inflation rate. This explains much of the surprise.

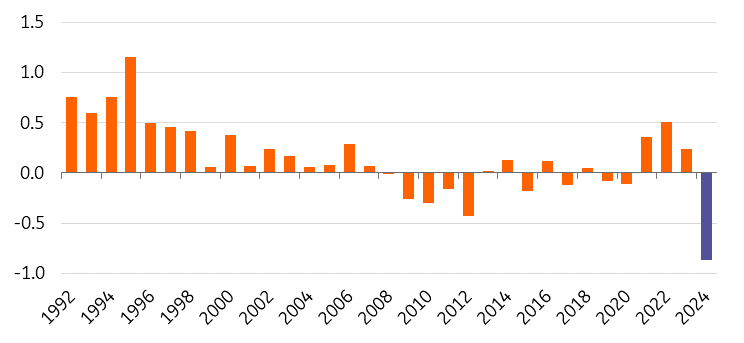

- Services prices on average fell by 0.9% MoM; the cheapening of other travel (mainly including airline ticket prices) and health services also contributed to this. Such a monthly decline in services prices has not been seen since the statistical time series became available in 1992. In fact, over the last three years, October has typically seen an increase of prices in the range of 0.2-0.5% MoM.

- Clothing prices rose more strongly on a month-on-month basis, which is a seasonal effect, but food prices also continued to rise, by 0.7% on a monthly basis. With regard to the latter, the drought, the weaker Hungarian forint and the ongoing price recovery after the removal of price caps could explain the price movements.

- Fuel prices rose by only 0.8% MoM in October, which was not surprising given the available data and statistical methodology. Though the perceived inflation here has been much stronger lately.

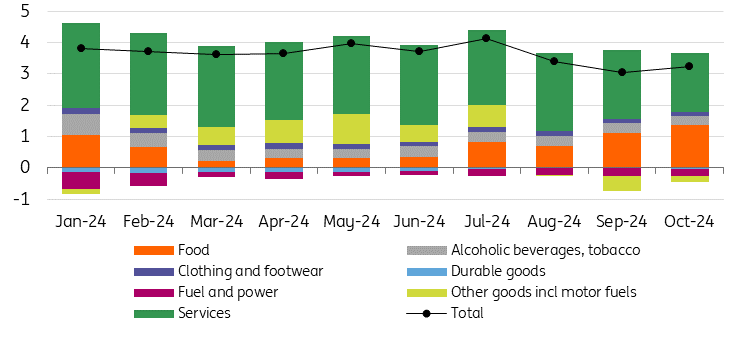

The composition of headline inflation (ppt)

Services and food prices drive inflation

The year-on-year inflation accelerated by only 0.2ppt in October compared with the previous month. There are two factors behind this pick-up in inflation. The first is the rise in food prices, which at 4.5% on an annual basis are well above average, and the highest food inflation seen so far this year.

Due to the low base, we still see an upward impact from fuel prices on an annual basis. Together, these two items alone would have added 0.5ppt to the inflation rate (bringing inflation to 3.5% YoY, exactly in line with market expectations), but this was offset by a large surprise fall in services prices. The year-on-year change in services prices is now 'only' 7.2%. In very simple terms, then, we can say that the yearly-based inflation rate is being driven by two factors: higher services prices and higher food prices.

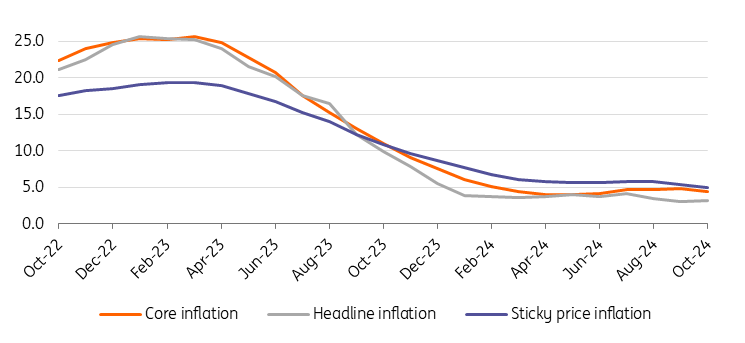

Headline and underlying inflation measures (% YoY)

Inflation to accelerate temporarily

Looking ahead, inflation is expected to rise further in the next two months. On one hand, this is due to the low base – and on the other, monthly reassessments are likely to become more pronounced again. In the coming months, we are unlikely to see a similar drop in the prices of, for example, telecommunications or health services.

It may well be that the sharp fall in recorded prices for telephone and internet services reflects the impact of the free data packages offered during the September floods, which may have been recorded by the Statistical Office (HCSO) in October (the billing period). If this is indeed the reason, the HCSO is expected to record a significant increase in this item in the coming period (probably in November), which could push up the monthly inflation rate by 0.2ppt.

Monthly price changes for services in October (%)

In addition, fuel prices will push up the general price index in the coming months, the depreciation of the HUF may stimulate imported inflation (mainly via durable consumer goods) and food prices may continue to rise. As the rise in fuel and food prices is an important amplifier of perceived inflation, the favourable official statistics will not help to dampen households' cautionary motives and fears of inflation towards the end of the year. Inflation expectations may therefore start to rise again, creating further headwinds for the Hungarian National Bank.

For the year as a whole, headline inflation could average 3.6%, while we expect slightly higher inflation next year (around 3.6-4.0%, according to our preliminary estimates). How much inflation will eventually pick up will depend to a large extent on the HUF exchange rate, wage growth and the repricing power of corporates. The latter will also be an important factor in next year's tax increases.

FX instability will drive monetary policy decisions

Overall, the data release was favourable for Hungarian monetary policy, mainly due to the slowdown in year-on-year core inflation. However, perceived inflation and the expected rise in inflation expectations would in themselves call into question the continuation of interest rate cuts. But such an issue (monetary easing) is hardly something that should concern policymakers nowadays, given the forint's woes.

The big question remains whether the central bank will start communicating openly in November about the possibility of raising interest rates if the circumstances require it. While it would seem logical to slip this in at the November meeting, it could well be that the central bank is drawing in investors by encouraging them to test the NBH's breaking point and tolerance for exchange rate weakness. In other words, the Monetary Council could be putting itself in the crosshairs. So monetary policy is not in an easy position, and the weakening of the forint is likely to continue in the coming days and weeks.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap