- Quick take

Turkey’s current account deficit remains on a widening track

- 13 February 2026

- Turkey

December's current account deficit in Turkey turned out significantly wider than expected, maintaining a gradual increase on a 12-month rolling basis. Meanwhile, the capital account has remained weak, leading to reserve depletion

Turkey's current account posted a deficit of US$7.3bn, higher than the market forecast (US$5.3bn) and our call (US$5.5bn). As a result, the 12-month rolling current account deficit maintained the uptrend and reached US$25.2 bn, or approximately 1.8% of GDP, from US$22.7bn a month ago.

A closer look at the monthly figures shows that the deficit widened by roughly US$2.5bn compared to the same month of 2024, primarily due to a higher trade gap, which deteriorated from US$-6.2bn to US$-7.4bn. In addition to the turn of the core trade surplus in 2024 to a deficit – weighing on foreign trade and, in turn, the current account – this deterioration in the monthly current account was also driven by a worsening balance in primary income. However, lower energy and gold deficits limited the deterioration in the current account balance.

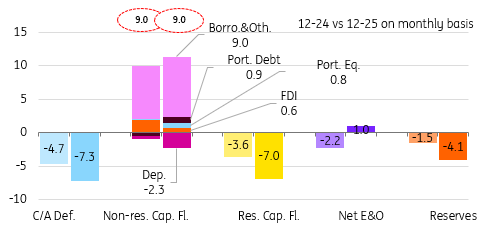

On the capital account side, inflows remained weak in December at US$2.1bn. With net inflows from errors and omissions of US$1.0bn, and considering the current account deficit, official reserves contracted by US$4.1bn.

Further analysis reveals that resident activities generated an outflow of US$7.0bn, mainly due to several factors, including outward FDI, portfolio investments, extending trade credits and increasing deposits abroad. On the flip side, non-resident activity led to inflows totalling US$9.0bn, primarily from debt-related channels.

Accordingly, despite a US$2.3bn fall in foreign deposits in local banks, a US$6.0bn net borrowing trade credit at US$2.7bn and portfolio inflows amounting to US$1.8bn turned out to be the major contributors to a positive capital account. In the breakdown, banks’ borrowing stood at US$1.3bn, while corporate borrowing was strong at US$4.3bn, with a large share in the long-term. Consequently, long-term debt rollover ratios stood at 377% for corporations and 113% for banks, compared to 202% and 184%, respectively, on a 12-month rolling basis.

In 2025, resident outflows rose to US$44.2bn from US$35.4bn a year ago. Foreign inflows, on the other hand, recorded an increase, coming in at US$64.2bn compared to US$57.8bn in 2024. As a result, the capital account has remained in positive territory with US$19.8bn, compared to US$22.3bn.

In addition, outflows via net errors and omissions remained elevated, totalling US$-16.6 bn vs US$-11.3 bn in 2024. Taken together with the widening current account deficit, which grew from US$-10.4bn to US$-25.2 bn, official reserves were depleted by US$22.0bn vs a slight US$0.6bn increase recorded a year earlier.

Overall, the current account surplus in December exceeded expectations and maintained a widening trend, while the capital account has remained weak, which has been the case since July. Preliminary customs data from the Ministry of Trade suggest continuing deterioration in the January current account, as the foreign trade deficit appears to be widened by US$0.8bn in comparison to last year.

In the months ahead, the trajectory of the current account balance is expected to be influenced by a mix of external risks – such as global trade developments and geopolitical tensions – alongside domestic demand conditions. We expect a modest widening this year, while capital inflows will likely remain sluggish amid significant outflows via net errors and omissions.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more