- Quick take

- 12 February

- Hungary

Why we can’t ignore Hungary’s rate cut-triggering low inflation

Inflation in Hungary came in as expected in January, well below the central bank’s target level. The favourable trend continued in the pattern of monthly repricing. The structure also shows some improvement, so the chance of a February rate cut is higher than ever

| 2.1% |

Headline inflation (YoY)ING estimate 2.0% / Previous 3.3% |

Inflation rate dipped sharply

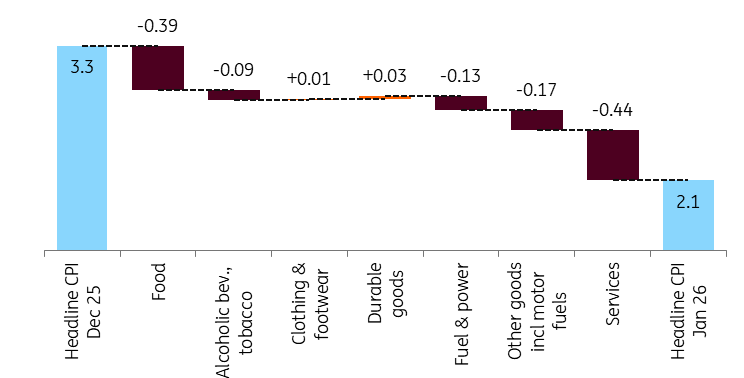

Hungary's inflation rate fell sharply in January 2026, according to recent data released by the Hungarian Central Statistical Office (HCSO). This time, favourable developments can be seen in almost every aspect. The year-on-year inflation rate of 2.1% was lower than the market consensus but came close to our forecast. Prices rose by only 0.3% on a monthly basis, which is significantly lower than the usual monthly repricing at the beginning of the year. The 1.2ppt slowdown in the year-on-year indicator compared to December is due to both low monthly repricing and the base effect.

Main drivers of the change in headline CPI (%)

The details

- In line with global food price trends, the monthly price adjustment in January was moderate at 0.6%. Lower producer prices are filtering into consumer prices, partly due to the margin freezes in selected food products.

- Despite the strong forint, inflation in durable consumer goods was unusually high. However, it was mainly the prices of products requiring precious metals in their manufacture that rose. The rising cost of raw materials may have been reflected in the prices of these products.

- Household energy prices fell on a monthly basis, primarily due to the cost of piped gas. The 1.5% decline in fuel prices also contributed significantly to the low average inflation rate. The forint's significant strengthening against the dollar, coupled with moderating oil prices, helped drive down the price of this product group.

- Inflation in the services sector also showed favourable signs; it was significantly lower than the average monthly price increase since 2010, at just 0.4% in January. Of course, there are items where inflation is still hot, but 5% year-on-year inflation is the lowest in five years.

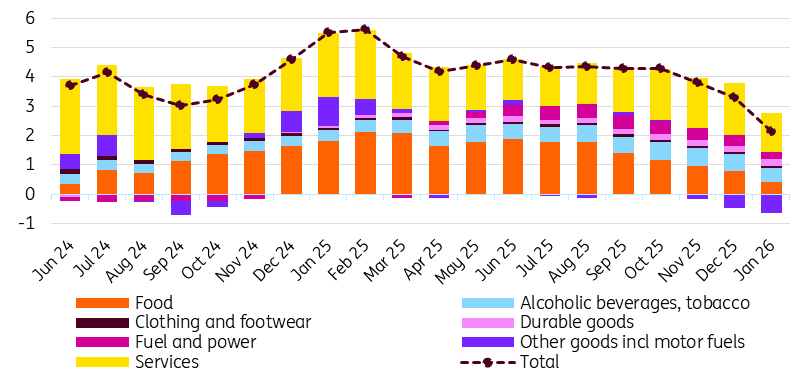

The composition of headline inflation (ppt)

Core inflation showing positive signs

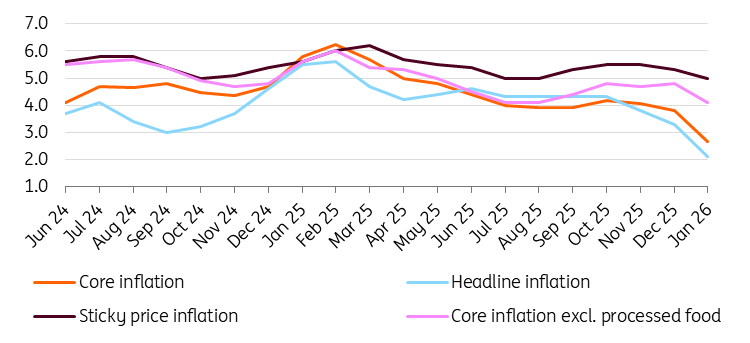

The core inflation rate, which is adjusted for volatile items, also developed favourably, falling to 2.7% on a yearly basis. This is the first time since January 2019 that both core and headline inflation rates have fallen below the central bank's 3% target. Of course, we know that low inflation is partially artificial due to the government’s price shield measures and some delayed tax and excise duty hikes. However, core inflation adjusted for indirect taxes also moved to 2.6% YoY. In its assessment, the National Bank of Hungary tried to be balanced when analysing the January inflation print. One of the key messages is that inflation expectations of households remained above the level of expectations seen during the period of price stability (2017–2020).

Headline and underlying inflation measures (% YoY)

The door to a February rate cut are wide open

However, if these low inflation prints are maintained in the coming months, then consumer inflation expectations may finally start to decline significantly, in our view. This is particularly likely if inflation continues to moderate further in February, as we expect it to hit the 1.5% mark (or come close to that). Furthermore, the indicator may remain low in the coming months as price shield measures have been extended by three months once again.

Based on this, the expected reacceleration in inflation will also be delayed until later in 2026. This means that inflation is increasingly likely to average around 3% for the year as a whole, in contrast to our recent 3.3% forecast.

Headline and core inflation falling below 3% in January, favourable service inflation, extended price measures, a strong forint and the market pricing in interest rate cuts in February and March clearly set the direction for monetary policy. In our opinion, the central bank may cut the base rate by 25bp in both February and March. The only case we see this not materialising is if another significant geopolitical event causes a sustained weakening of the forint in the coming weeks.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more