- Quick take

- 13 May 2019

- Turkey

Turkey: Current account deficit narrows further

The external deficit continued to recover in March, while the outlook for capital flows has remained weak, leading to a decline in reserves

| $13.4bn |

C/A deficit(12M rolling, as of March) |

Weaker domestic demand and increased price competitiveness, along with strength in tourism, have led to an improvement in Turkey's external balance, which has been adjusting from a period of volatility last summer. In March, the monthly deficit stood at $-0.6 billion, better than the market consensus at $-1 billion (and our call at $-1.1 billion), while the 12-month rolling current account deficit recovered further to $-13.4 billion, the lowest in 10 years. The fall in the deficit has been rapid, dropping from $-58.1 billion over a period of just 10 months.

External Balances (USD bn, 12M rolling)

The monthly improvement over the same period of 2018 is again attributable to a contraction in foreign trade, along with relatively small supportive impacts from services, primary and secondary incomes.

On the financing front, following a relatively better flows outlook in the first two months of the year due to Treasury issuances, capital flows weakened again in March to $-0.8 billion. Given the mild external deficit and significant outflows of $4.3 billion via net errors & omissions, official reserves recorded a $5.7 billion decline, the first since September.

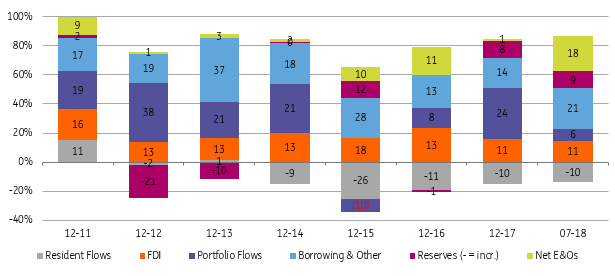

Breakdown of C/A Financing* (12M Rolling, USDbn)

* Positive sign in reserves shows reserve accumulation

Capital outflows are mainly attributable to a rise in the currency and deposit assets of banks, at $4.7 billion in March, while on a 12-month rolling basis, the figure is $18.5 billion. It seems that banks continued to transfer FX to their corresponding banks abroad.

Regarding borrowing, banks have remained net payers (US$-0.7 billion, driven mainly by long term repayments. This translates into a monthly rollover ratio of 62% vs a 12M rolling figure at 73%). However, this was more than offset by corporate sector borrowing at $0.8 billion (thanks to long term borrowing at $1.0 billion with monthly 12M rolling rollover ratios at 159% and 127%, respectively).

Portfolio flows painted a mixed picture, with non-residents selling $0.6 billion in the equity market and $0.9 billion in the bond market while net issuance of the Treasury, after heavy activity in the previous months, was $-0.5 billion. However, banks which managed to issue $1.7 billion of bonds on the international markets almost balanced the outflows through the other items.

Net FDI at $1.0 billion and a $0.9 billion increase in non-residents’ deposits held at local banks, contributed to monthly inflows.

The ongoing rapid correction in external imbalances, with a sharp reduction in the current account deficit (thanks to plunging domestic demand and increased competitiveness) will likely continue in the first half of this year before rising gradually in the second half. Outflows accelerated in March, signalling that the outlook will remain challenging, driven by market conditions as well. Sizeable financing needs will likely keep Turkey sensitive to shifts in global risk appetite.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more