- Quick take

- 14 June 2019

- Turkey

Turkish current account deficit narrows in April

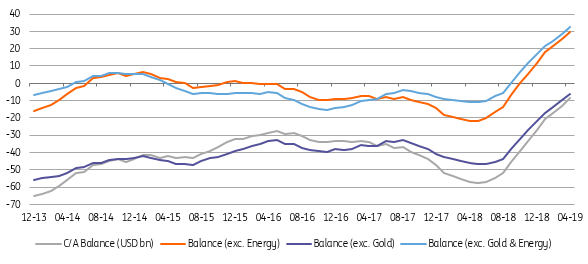

Turkey's external deficit narrowed in April, with the 12-month deficit down to just USD 8.6 billion, from USD 57.1 billion a year ago. However, the outlook for capital flows weakened further with a decline in reserves

| $-8.6bn |

Current account deficit12-month rolling, as of April |

External balances have maintained the recovery trend on the back of weaker economic activity and increased price competitiveness, while the contribution from tourism has helped.

With the April deficit standing at USD-1.3 billion, better than the market consensus of USD-1.5 billion, the 12-month rolling current account deficit narrowed further to US$-8.6 billion - the lowest since early 2004, from US$-58.1 billion over a year ago.

In the breakdown, the monthly improvement over the same period of 2018 is down to contraction in foreign trade, along with relatively small supportive impacts from services and primary incomes.

External Balances (USD bn, 12M rolling)

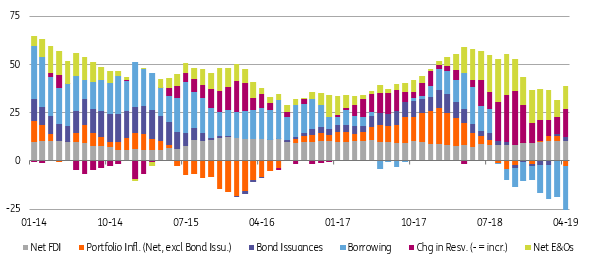

On the capital account, capital flows that turned negative in March due to increasing concerns about the central bank of Turkey reserves weakened further in April with US$-5.2 billion. Given mild external deficit and a significant US$3.8 billion inflows via net errors & omissions fully reversing the same amount of outflows a month ago, official reserves recorded US$2.8 billion decline.

In the breakdown, capital outflows are mainly attributable to increasing assets of residents abroad with the acquisition of US$2.4 billion financial assets mainly by corporates and a rise in the FX currency and deposit assets of banks at US$3.1 billion in April. So, it seems residents have kept acquiring assets abroad, amounting to US$32 billion on a 12-month rolling basis, driven mainly by transfer of FX by banks to their corresponding banks abroad at US$23.4 billion.

Breakdown of C/A Financing* (12-month rolling, USD billion)

* Positive sign in reserves shows reserve accumulation

Portfolio flows painted a mixed picture with non-residents selling a mere US$78 million in the equity market and US$0.7 billion in the bond market while net issuance of the Treasury after a heavy activity in the previous months was US$-1.4 billion. However, banks managed to issue US$0.5 billion bonds.

Regarding borrowing, banks have remained net payers with US$-0.8 billion (driven by US$1.1 billion long term repayments translating into a monthly rollover ratio at 74% vs 12M rolling figure at 67%), while corporate sector borrowing was slightly positive at US$0.2 billion (thanks to short term borrowing, while net long term financing was almost flat at 103% monthly rollover ratio vs 130% on 12M rolling basis).

Finally, net foreign direct investment is at US$0.6 billion and US$1.2billion increase in non-residents’ deposits held at the local banks were contributed to monthly inflows.

Overall, the correction in external deficit on the back of weak domestic demand and increased competitiveness will likely continue in the period ahead albeit at a slower pace. Outflows accelerated in April, signalling that outlook will remain challenging.

The global backdrop of increasing market expectations of Federal Reserve rate cuts given weakening prospects for global trade and global investment can impact countries like Turkey.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more