Inflation in Turkey was better than expected in March

Inflation in Turkey last month came in below consensus but despite some improvement in the underlying trend, the data showed continuing pricing pressures in non-food groups, confirming the challenges to the disinflation process

Inflation at 3.16% month-on-month was lower than the consensus (3.6%) and our call (4.1%), resulting in annual inflation of 68.5% year-on-year, up from 67.1% a month ago due mainly to the impact of non-food prices. While there was an increase of 2.3% in March 2023, the average of March months in the 2003-based index was 1.1%, indicating that the base effect was favourable for this year. However, the outcome was the second-highest March reading in the current series. Accordingly, cumulative inflation in the first quarter stood at 15.1% vs the 36% Central Bank of Turkey forecast for this year.

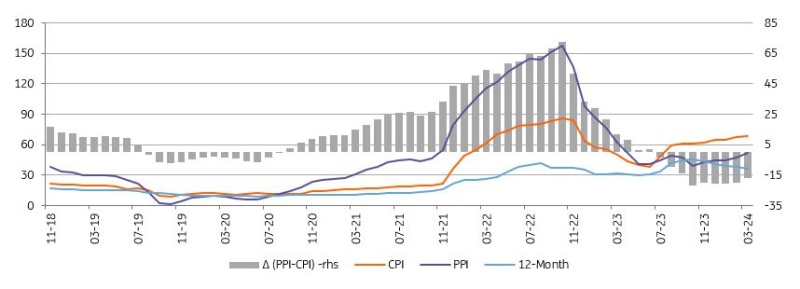

PPI, on the other hand, stood at 3.3% MoM, showing an acceleration to 51.5% YoY, the highest in a year. The data implies building cost pressures due to commodity price changes and exchange rate developments.

Inflation outlook (%)

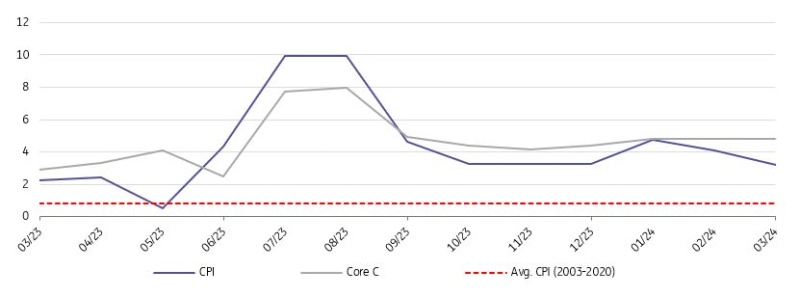

Core inflation (CPI-C) came in at 3.5% MoM, moving up to 75.2% on an annual basis on the back of pricing behaviour, implications of recent exchange rate developments, inertia in services, still resilient domestic demand, and ongoing deterioration in pricing behaviour. On a seasonally adjusted basis, after the spike in January, core inflation has remained elevated owing to second-round effects from wage hikes and administered price hikes. However, as pointed out by the central bank in the MPC minutes, the underlying headline trend showed an improvement thanks to the goods group, while services maintained their uptrend, confirming the challenges for disinflation.

As a result, monthly headline inflation (seasonally adjusted) dropped to the 3-3.5% range but remained elevated. The CBT sees seasonally-adjusted monthly inflation as hovering below 4% on average in the first half of this year (around 3% except for January). This implies that the disinflation should be more pronounced in the coming months for the forecast to hold.

Monthly trend CPI

Seasonally adjusted, Month-on-Month

In the breakdown, all groups with the exception of alcoholic beverages and tobacco provided positive contributions. Food again turned out to be the major contributor at 0.87ppt, though the annual figure moderated to 70.4% driven by both relatively benign unprocessed and processed food. Housing followed food with a 0.48ppt contribution due to continuing pressure in rent and adjustments in utility fees. Catering services, transportation, household equipment and education were other groups that lifted the headline by 25-35bp each. As a result, goods inflation moved up to 58.2% YoY, while core goods inflation inched up to 56.5% YoY. Annual inflation in services maintained its uptrend and reached another peak at 96.5% YoY mainly due to rent and telecommunication services.

Annual inflation in expenditure groups

Overall, the acceleration in the USD/TRY increased to around 4% in March due to the high FX demand before the municipal local elections. The recent upside pressures in commodity prices and domestic demand-related effects have kept the monthly inflation trend elevated in March, despite some improvement over the previous month. Additionally, the negative pricing behaviour in recent months and, most importantly, the inability to break high inflation expectations make it difficult for inflation to converge to the CBT’s 2024 target. In the near term, April and May inflation data will be in focus to assess the implications of the recent CBT tightening. Given this backdrop, the CBT will likely maintain its tight stance and keep the funding costs high, close to the upper band of the interest rate corridor.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap