- Quick take

Turkey: Trade deficit more than doubles in January

- 28 February 2018

- Turkey

The trade balance came in at USD9.1bn in January, while the 12M rolling deficit stood at USD81.5bn, continuing the expansion since early 2017, amid rising gold imports and energy bills as well as recently accelerating core imports

The foreign trade deficit in Turkey more than doubled in January to USD9.1bn, while the 12M rolling deficit, on a gradual uptrend since early 2017, continued to widen to USD81.5bn- the highest since Mar-15. Coverage of imports by exports on a 12M rolling basis, which has followed a downtrend in recent months, dropped further to 66.0%.

Three drivers of the significant increase in the trade deficit last year have remained in place:

- First, energy bills that have been going up since the end of 2016 with higher oil prices increased further in the first month of 2018, though energy imports lost some momentum over the previous month.

- Second, the deterioration in net gold trade continued--gold imports surged to an all-time high in 2017 and another record level was seen in January.

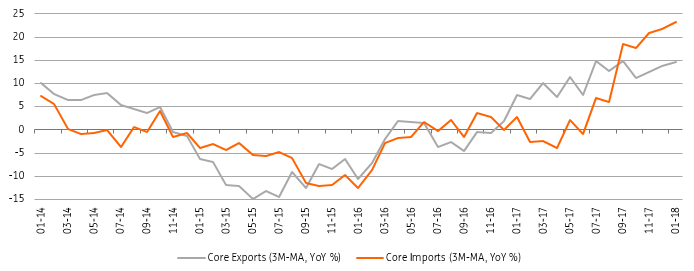

- And lastly, core imports excluding gold and energy also doubled in January on a YoY basis, showing the impact of ongoing strength in domestic demand, while the 12M rolling figure maintained the uptrend observed in the second half of 2017.

Accordingly, imports saw 38.0% YoY growth (translating into a 5.5% sequential increase). On the flip side, exports continued their healthy increase, by 10.7% YoY (with a 1.1% MoM rise) on the back of strength in EU demand and recovering trade with Russia. Improving Turkish lira competitiveness should also be a supporting factor for the performance of exports.

Overall, cyclical developments i.e. deteriorating net gold trade, a growing energy deficit and strong activity supporting core imports, have remained the major drivers for external balances. In 2018, whether we will see a normalisation in gold imports is difficult to judge but higher oil prices and likely solid domestic demand, with policymakers’ inclination to keep growth competitive, will keep the foreign deficit elevated.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more