- Quick take

Tough outlook for UK retailers despite June sales bounce back

- 18 July 2019

- United Kingdom

June’s bounce in retail sales has to be viewed in the context of monthly declines in April and May. While higher real wages should help spending in the near-term, the effect of Brexit uncertainty makes for a tricky outlook for retailers in the second half of the year

At face value, June’s 0.9% bounce in UK retail sales (excluding fuel) suggests that the better real wage growth backdrop may be translating into stronger demand among shoppers.

However it’s worth noting that June’s rise follows two consecutive month-on-month declines during April and May. The underlying drivers of June’s increase were also fairly mixed – second-hand stores reportedly were one of the best performers, while department stores saw the sixth consecutive month-on-month decline in sales.

This latest rise also doesn’t quite tally with the messages from the British Retail Consortium and other data providers, whose data suggests June was another sluggish month for the high street.

In principle though, the better fundamental outlook for spending should lift spending over coming months: wage growth is continuing to perform solidly, while the inflation backdrop looks relatively benign. However sentiment among consumers remains depressed and surveys point to particular concerns surrounding the general economic situation.

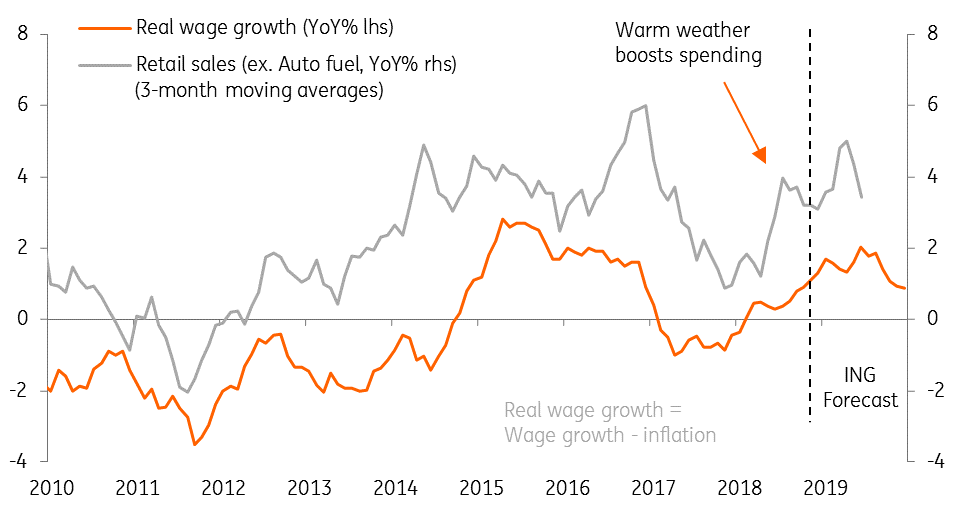

The real wage backdrop is looking brighter

If this uncertain backdrop continues to weigh on the consumer spending story, this could make for a tough time for retailers. Margins are likely to be squeezed further as firms make preparations for a possible ‘no deal’ Brexit at the end of October.

This is a costly process, not just in terms of working capital requirements, but also in terms of warehousing. According to the UK Warehousing Association, the inner-M25 (London) area has a vacancy rate of just 2.2%. For many, this will make it tricky to source the necessary space to store extra stock, and could complicate efforts to build inventory ahead of key Black Friday and Christmas trading periods.

As we discussed in our jobs report review, we think the fact that wage growth has been accelerating means it is too early to be discussing rate cuts in the UK (markets are now pricing a 50% chance of easing this year). But equally, with Brexit uncertainty set to weigh on both consumer and business activity over coming months, we think monetary tightening is also pretty unlikely during 2019.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more