- Quick take

- 6 March 2024

- United States

The Fed wants more data before cutting, but a cooling jobs market will help

Fed Chair Jay Powell's testimony to Congress suggests an inclination to cut interest rates to a more neutral level, but with inflation still above target and the activity data beating expectations, the central bank isn't in a position to do so. More data is required, but with more evidence of a cooling jobs market we still think they can cut rates from June

Fed's Powell inclined to cut rates this year, but needs the data to justify it

There was nothing particularly surprising within Fed Chair Powell's prepared monetary policy testimony to Congress - which is pretty short in fairness – or the Q&A session. The main comments are that "the risks to achieving our employment and inflation goals have been moving into better balance", with a reiteration that Fed members "believe that our policy rate is likely at its peak for this tightening cycle".

If the economy continues to make progress towards the Fed's goals, as expected, then it will probably "be appropriate to begin dialling back policy restraint at some point this year. But the economic outlook is uncertain, and ongoing progress toward our 2 percent inflation objective is not assured." So a similar message to other Fed officials in that they are inclined to cut rates later this year, but need to see more evidence to justify that action.

We think it will come given the evidence of a cooling jobs market (see below) and the prospect that weak real disposable household income growth, the exhaustion of pandemic-era accrued savings and high borrowing costs putting more stress on household finances will result in weaker consumer spending. This, in turn, should continue to dampen price pressures in the economy. We forecast a first interest rate cut at the June FOMC meeting.

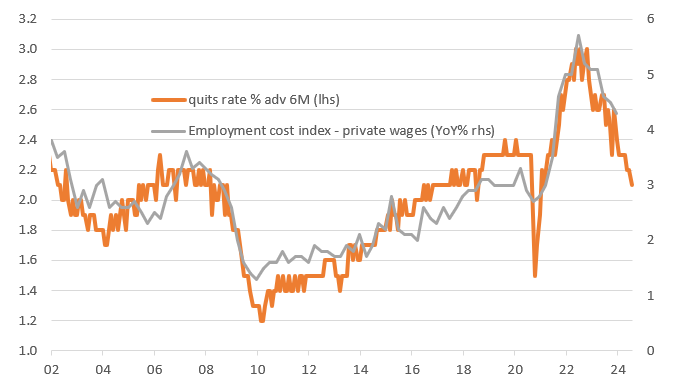

Falling quits ratio suggests a cooling jobs market

Today’s main data report was the Job Opening and Labour Turnover Statistics (JOLTs). The US job openings (vacancy) data is broadly in line with expectations, with openings coming in at 8863k versus a downwardly revised 8889k in December. The consensus was 8850k. This is basically tracking the Indeed job website data and looks set to slow further in February towards 8500k.

We are more interested in the quit rate - the proportion of workers quitting their job to move to a new employer each month - and that slowed to 2.1% from 2.2%. It had been as high as 3% in 2022. This slowdown suggests that while there are still lots of vacancies out there, they aren't especially attractive and fewer and fewer people are interested in taking them. This has a knock-on effect in that if there is less labour market churn there is less need for an employer to pay up to retain staff.

Falling quits ratio suggests more heat is coming out of the jobs market with cost pressures set to ease further

The chart above shows the relationship with the employment cost index - the broadest and best measure of labour costs since it includes bonuses and benefits - and it suggests an ongoing cooling, which should delight the Federal Reserve. It suggests that inflation pressures from the jobs market are normalising despite unemployment being low.

With regards to Friday’s jobs report, the falling quits rate coupled with both the manufacturing and service sector ISM employment indices being in contraction territory, plus the ADP private employment report posting a sub-consensus 140,000 increase (and the seventh consecutive reading between 104-158,000) suggests that we must surely see a slowdown in nonfarm payrolls growth. After 333,000 and 353,000 prints for December and January, respectively, economists are pencilling in a 200,000 forecast but given the propensity for official data to come in far hotter than survey and anecdotal evidence, confidence is low in this prediction.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more