- Quick take

The Commodities Feed: The OPEC+ dance

- 5 March 2020

- Commodities daily

Your daily roundup of commodity news and ING views

Energy

The key OPEC+ meetings get underway in Vienna today, and this follows the Joint Ministerial Monitoring Committee gathering yesterday, where a handful of ministers tried to at least move towards a preliminary agreement. As usual, and probably widely anticipated, the sticking point continues to be between what Saudi Arabia and Russia want. Media reports suggest that Saudi Arabia wants to cut by as much as 1.5MMbbls/d more in 2Q20, along with extending the existing deal through until year-end. On the other hand, Russia appears to favour extending the current deal, rather than making deeper cuts. The price action in ICE Brent yesterday was pretty clear - the market will be disappointed with just an extension. We continue to believe that the group will need to cut by levels that the Saudis are wanting, particularly in the current environment, where there is a continued downside risk to demand.

Meanwhile moving away from OPEC+, and the prompt ICE Brent time spread swung back into contango yesterday, with the May/Jun spread settling at a US$0.12/bbl discount, this compares to a backwardation of US$0.15/bbl on Monday. This is a sign of a looser prompt physical market and ties in with reports of a large volume of unsold West African cargoes amid weaker refinery margins.

Finally, the EIA reported yesterday that US crude oil inventories increased by just 784Mbbls, far less than the 3MMbbls build the market was expecting. Meanwhile larger than expected draws were seen on both the gasoline and distillate fuel oil side. The large product draws did provide some strength to cracks. Overall the report was fairly constructive, with total oil and refined product stocks declining by 11.9MMbbls, which is the largest weekly decline since June. On the trade side, crude oil exports surged to 4.15MMbbls/d over the week (+497Mbbls/d WoW), which is the second-largest export number seen from the US. This helped the US remain a net exporter of oil and product for the third consecutive week.

Metals

The performance of the PGMs complex remains a mixed bag, with the platinum/palladium ratio continuing to sink. This is despite the World Platinum Investment Council (WPIC) estimating in its latest quarterly release a more balanced market for platinum this year, by reducing its previous supply surplus estimate of 670 koz to a marginal surplus of 119 koz for 2020.

The automotive sector remains the largest driver for platinum demand, and the WPIC expects demand in this sector to reach 3 moz in 2020, compared to 2.89 moz in 2019. Although overall jewellery demand remains a drag for platinum, global platinum supply is expected to remain largely flat, reaching 8.1 moz in 2020. Declines in mine supply are expected to be offset by an increase in secondary output, which is expected to rise by 5% YoY to 2.1 moz. Admittedly, there is downside risk to these figures, given the impact from Covid-19. This is highlighted by Chinese vehicle sales over February, which fell by 80% YoY, according to the China Passenger Car Association.

Base metals traded mostly in positive territory yesterday. In the short-term copper remains buoyed by the easing we are seeing from central banks. Meanwhile, a Bloomberg survey shows that China is making a gradual improvement in work restarts, with the economy running at 60%-70% capacity last week, up from 50% during February. However, other anecdotal reports also pointed out that the rate of ramp-up could vary among different industries and also the size of organizations. For example, figures released earlier by CNIA shows that overall metals production is running at a much higher rate than the Bloomberg survey suggests. This helps to explain the inventory builds we have seen in metals recently, with downstream users yet to return to pre-Chinese New Year levels.

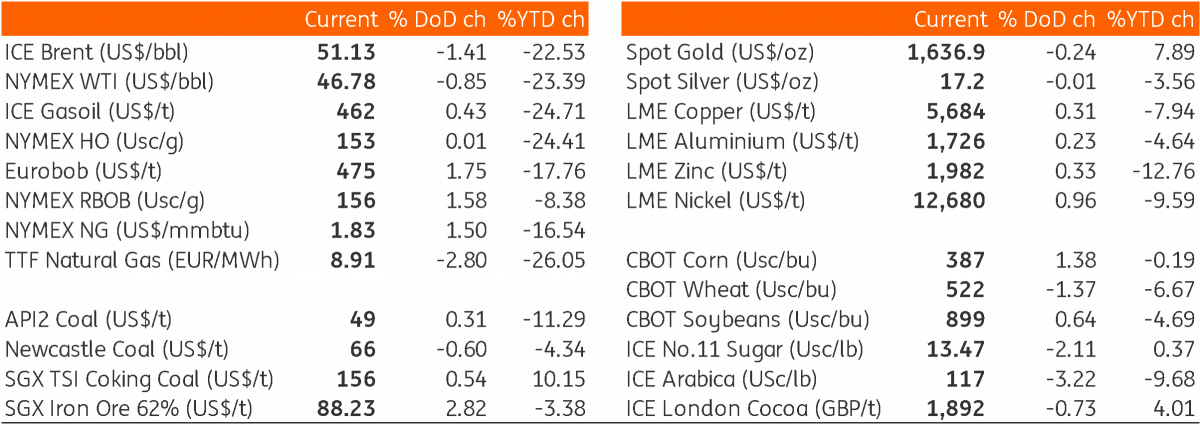

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more