- Quick take

The Commodities Feed: Sub $50/bbl jitters

- 2 March 2020

- Commodities daily

Your daily roundup of commodity news and ING views

Energy

The move lower in oil last week was relentless, with ICE Brent down almost 14% and the pressure has continued this morning, with ICE Brent briefly trading sub-US$50/bbl. Clearly the spread of Covid-19 has got market participants increasingly nervous over the impact on oil demand growth. Despite the aggressive sell-off in the market, speculative positioning in ICE Brent was little changed over the week. This is likely to be reflected in this week's report, with the bulk of the move lower occurring towards the end of the week, whilst the Commitment of Traders data only covered until Tuesday.

The more recent pressure on prices will likely be getting OPEC+ members more nervous and increasing the likelihood that they will take significant action at the OPEC+ meeting on Thursday and Friday this week. These price levels will even start getting the Russians a bit worried, as they move closer to their fiscal breakeven level. This ties in with comments from President Putin over the weekend, where he said Russia will continue to cooperate with OPEC. The key question though is how much will OPEC+ agree to cut. We believe that anything that falls short of the OPEC+ Joint Technical Committee recommendation of 600Mbbls/d of additional cuts over 2Q20, and extending the current deal through to year-end, will be taken as bearish. Meanwhile additional cuts of 1MMbbls/d over 2Q20 would likely be seen as constructive. While the demand uncertainty makes the job of OPEC+ difficult enough, the other challenge for the group is knowing where Libyan output will be as we move into the second quarter.

Metals

Industrial metals extended losses last week amid the continued global spread of the Covid-19 virus. While poor Chinese manufacturing PMI data out over the weekend will do little to improve sentiment in markets at the moment, with the reading for February the lowest ever on record.

A key observation for base metals is the continued inventory build, particularly in China. Copper stocks in SHFE warehouses increased by 12kt over the last week, with inventories now nearing a three-year high of 311kt. Inflows over February totalled 105kt versus 85kt over the same period last year. Meanwhile, SHFE zinc saw an increase of 17kt over the week to total 160kt, whilst SHFE aluminium stocks grew by 29kt to 439kt - the highest level since June 2019. The standout though is lead, where stocks declined over the week.

Meanwhile, recent data from the China Association of Automobile Manufacturers (CAAM) shows that automobile sales in China dropped by 18.7% YoY to 1.93M units in January. It also expects production and sales of automobiles to contract sharply in February following the outbreak of Covid-19.

Turning to precious metals, and gold was unable to escape the downward pressure that we saw across markets on Friday. This was a strange development given the usual safe-haven status of the metal. Reports, however, suggest that the sell-off in gold reflects the fact that investors had to liquidate gold positions in order to meet margin calls elsewhere. We believe the trend for gold remains unchanged, and that is upwards, given the level of uncertainty in markets at the moment.

Agriculture

The outlook for sugar prices continues to improve, with deficit forecasts for the global market continuing to grow. The International Sugar Organization now forecasts that the market will see a deficit of 9.4mt in the 2019/20 season, which compares to their previous forecast of 6.1mt from November. Revisions come on the back of poorer output from both Thailand and India. Meanwhile, export data from the EU Commission shows that sugar exports from the region fell 60% YoY to total just 355kt in the season so far.

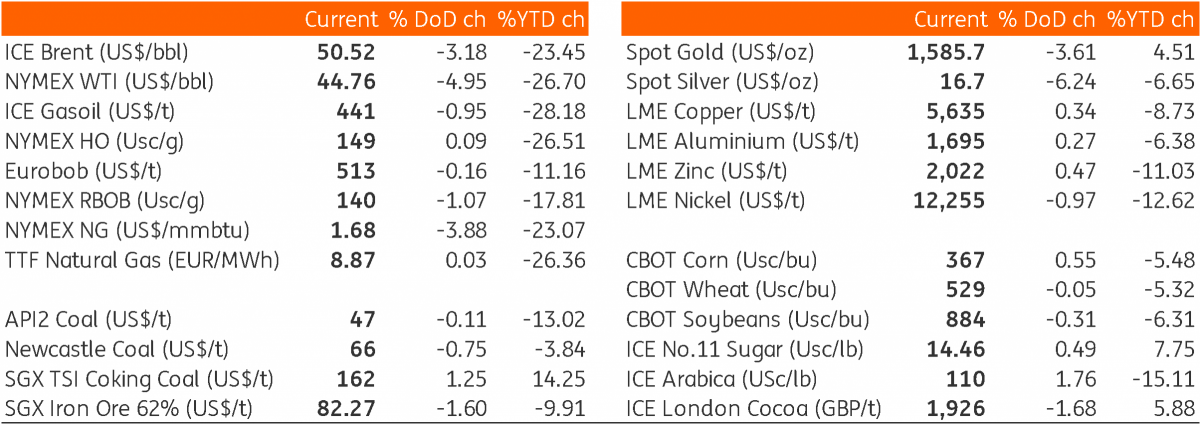

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more