- Quick take

- 13 February 2020

- Commodities daily

The Commodities Feed: OPEC revises demand lower

Your daily roundup of commodity news and ING views

Energy

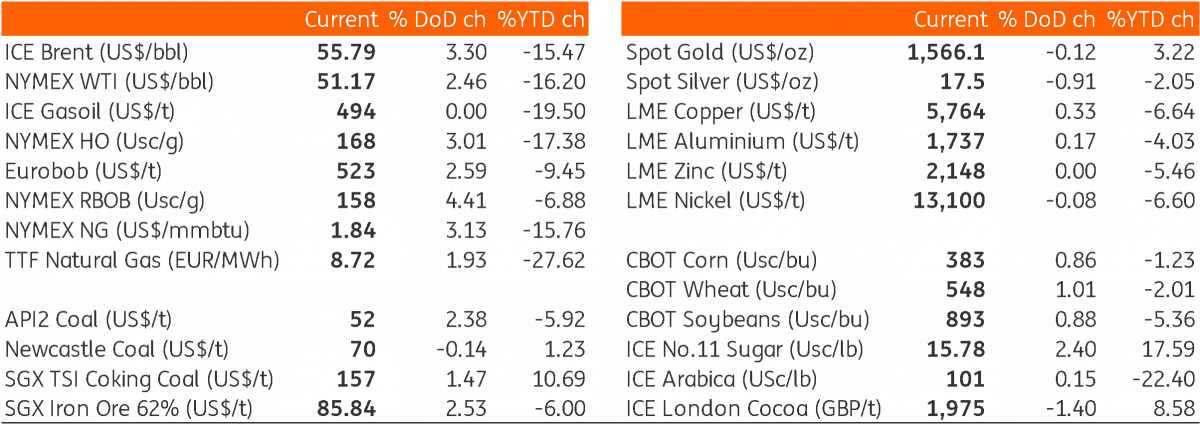

Optimism in the market continued yesterday, with ICE Brent settling 3.3% higher on the day. This was part of a broader move higher, as markets took comfort in the slowing growth of new COVID-19 cases. Strength in oil continued in early morning trading despite news that the number of cases in Hubei province jumped by almost 15,000 due to a broadening in the definition of how to diagnose the virus.

Meanwhile, yesterday OPEC released its monthly oil market report, where they revised lower their demand growth estimates for 2020 by 230Mbbls/d, which takes their demand growth forecast for 2020 to 990Mbbls/d. The demand revisions are weighted towards the first half of this year. OPEC numbers suggest that OPEC would need to cut production by 569Mbbls/d in 2Q20 from January output levels to keep the market in balance. Later today, the IEA will release their latest monthly report, and the market will be watching closely to see what revisions they make to demand as a result of the virus.

The EIA also released its weekly inventory report yesterday, which showed that US crude oil inventories increased by 7.46MMbbls over the week, which was more than the 3.2MMbbls build the market was expecting, and higher than the 6MMbbls increase the API reported the previous day. This is also the largest stock build seen since November. The build was largely driven by trade, with crude oil exports falling by 443Mbbls/d WoW, to average 2.97MMbbls/d- the lowest weekly export number since early November. In contrast, crude oil inflows increased by 363Mbbls/d.

Finally, products got a boost yesterday after a fire broke out at Exxon's 500Mbbls/d Baton Rouge refinery in Louisiana - the fifth largest refinery in the US. It is reported that all crude units at the refinery were shut down as a result. However, the company has not provided details on the status of all units at the refinery.

Metals

Base metals remained largely range-bound yesterday, despite weak industrial production data from the Euro area. Industrial output contracted the most in the past four years, falling 2.1% MoM in December, which was more than the 1.6% decline expected. Meanwhile, China’s central government yesterday ordered crucial industries and major construction projects to restart and return to normal working order as soon as possible.

In precious metals, Johnson Matthey yesterday released its half-yearly update, in which they estimate that the platinum market ended 2019 with a deficit of 203kOz, compared to a supply surplus of 420kOz the preceding year. Net demand grew by 9% YoY due to a sharp rise in investment demand, which picked up from 63kOz in 2018 to 1.3mOz in 2019; while jewellery and autocatalyst demand remained weak. Total supply remained weak, with the majority of declines coming from South Africa, where mine supply has struggled due to electricity shortages and wage negotiations last year. For 2020, platinum supplies could fall below 6mOz their lowest in six years due to constrained mine supply in South Africa and declining Russian supply. The platinum market may end 2020 with a supply deficit, following a muted supply outlook and potential upside in autocatalyst and investment demand.

Turning to palladium and the market is estimated to have seen a supply deficit of 1.2mOz in 2019 vs. a slight deficit of 77kOz in 2018. Net demand for palladium jumped 14% YoY to 8.1mOz, while total supply declined by 1.6% YoY in 2019. The main driver for the demand growth was autocatalyst demand, which picked up 10% YoY to reach 9.7mOz. For 2020, palladium is expected to encounter deeper supply deficits as automotive demand will remain strong and is expected to rise above 10mOz, following stricter emission regulations in China and Europe.

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more