- Quick take

- 6 August 2020

- Commodities daily

The Commodities Feed: Oil breaks out

Your daily roundup of commodity news and ING views

Energy

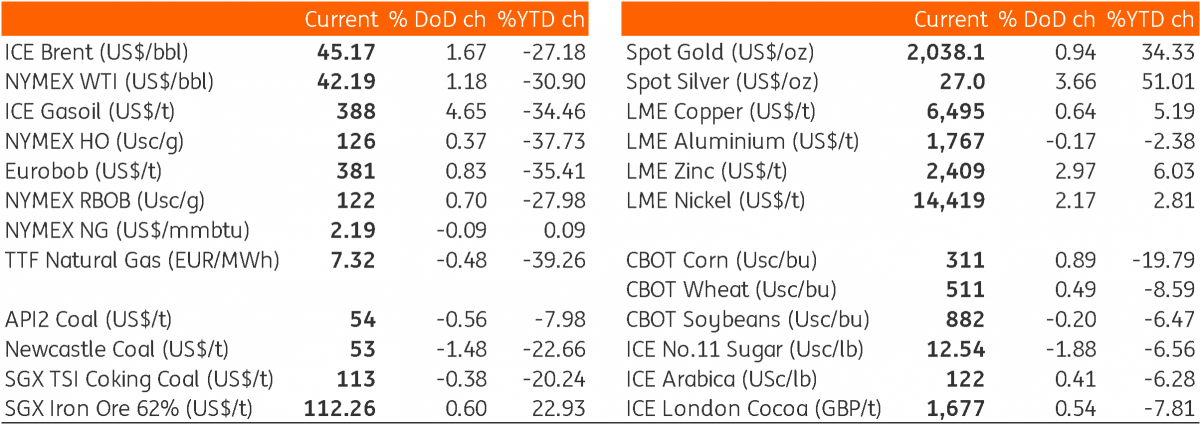

Oil finally broke out of the narrow range it has been trading in for over a month now, with ICE Brent trading as high as US$46.23/bbl at one stage yesterday, although the market was unable to hold onto all of these gains going into the close. The key drivers behind the move higher appear to be growing hopes for US stimulus, further weakness in the USD - with the dollar index falling to levels last seen in the first half of 2018, and the EIA reporting that US crude oil inventories declined by 7.37MMbbls over the last week- which was significantly more than the market was expecting.

However whilst we saw crude draws, the refined product market is looking less promising, with gasoline and distillate fuel oil inventories growing by 419Mbbls and 1.59MMbbls respectively. Distillate stocks stand at a little under 180MMbbls, which is more than 42MMbbls above levels seen at the same stage last year. Meanwhile, demand continues to struggle, with implied demand for total products falling by 1.18MMbbls/d over the week. It is difficult to get overly constructive towards the oil market with demand having stalled and this product overhang.

Finally, Saudi Aramco are expected to release their official selling prices (OSP) for their crude oil in September. Expectations are that the Saudis will cut their OSP for crude oil into Asia for the month, following the easing in supply cuts from OPEC+. The OSP for Arab Light into Asia for August is US$1.20/bbl above the benchmark.

Metals

Silver remains the outperformer among the metals complex, rising by more than 3.6% yesterday with the gold/silver price ratio falling to a two year low of below 76. Silver prices have increased by around 48% since the start of 3Q20. In addition to strong investment demand for precious metals on account of falling Treasury yields and an increase in geopolitical risks, silver prices were further supported by the sharp recovery in industrial activity across the globe. Meanwhile, mined supply remains relatively constrained due to disruptions in Peru and Mexico.

Base metals continued their positive run yesterday on the back of hope around fresh economic stimulus from the US, while a weaker USD provided further support. The Philippines has implemented a stricter two-week lockdown in some parts of the country, which saw nickel prices closing more than 2% higher on the day on supply concerns. Chinese refined nickel output dropped by 3.1%MoM to 14.6kt in July, according to SMM data, providing further support to nickel.

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more