- Quick take

The Commodities Feed: Iron ore rally

- 19 June 2019

- Commodities daily

Your daily roundup of commodity news and ING views

Energy

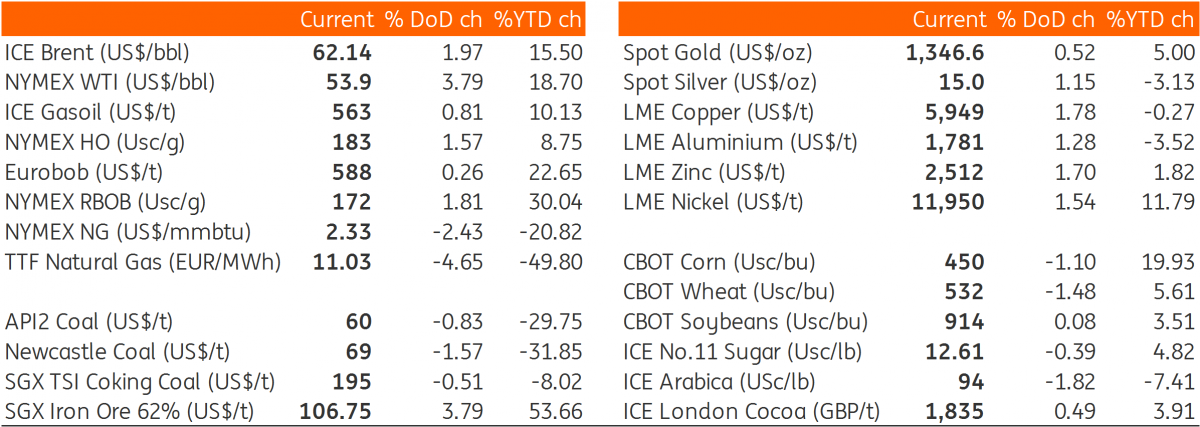

US oil numbers: The API reported yesterday that US crude oil inventories fell by 812Mbbls over the last week, not too far off from the 1.25MMbbls drawdown that the market was expecting according to a Bloomberg survey. Meanwhile, the API also reported that gasoline inventories increased by 1.46MMbbls, while distillate fuel oil inventories fell by just 50Mbbls. The EIA is scheduled to release it more widely followed report later today, and confirmation of stock drawdowns could offer further support to the market, following the rally yesterday, after reports that China and the US will meet during the G-20 summit in Japan next week, where they will resume trade talks.

OPEC+ meeting: While OPEC members continue to work towards an agreeable date for their mid-year meeting, OPEC’s Economic Commission Board has said that if the group was to continue with their production cut deal over the second half of the year, that oil inventories would fall by 500Mbbls/d, according to a Bloomberg report. Although this will be largely dependent on how demand growth plays out for the remainder of the year. Both OPEC and the IEA are forecasting that demand growth will pick up in the second half of this year, after a sluggish Q1, however, the risk is if we end up seeing further deterioration of the macro picture. Finally on the OPEC+ meeting, according to media reports, the latest proposed dates are the 1-2 July.

Metals

Iron ore strength: The SGX July 2019 iron ore contract continues to strengthen, with prices breaking above US$108/t this morning- the market has rallied almost 14% since the start of June. The latest from Brazil is that Vale’s 30mtpa Brucutu mine could remain closed for longer, with the company yet to make a deal with prosecutors and regulators on the mine restart.

Chile mine strike: Strike action at Codelco’s 320kt pa Chuquicamata mine in Chile entered the fifth day yesterday with some violent clashes reported at the mining site between police and striking workers. The mine has been operating at nearly half of its capacity due to the strike, and violent clashes could push operating rates down further if striking workers block mine access. Disruption to concentrate supply could put further downward pressure on spot treatment charges, with them already having fallen 30% in China so far this year.

Agriculture

White sugar premium pressure: The Aug/Jul whites premium has been under pressure for much of the month, falling from around US$67/t towards the end of May to below US$55/t earlier this week. What hasn’t helped over the month, is the sheer size of sugar stocks in India, with the Indian Sugar Mills Association (ISMA) estimating that sugar stocks will stand at 14.62mt at the start of the 2019/20 marketing year, which starts on the 1st October. ISMA believe that India should target 7mt of exports in 19/20, up from an estimated 3mt in the current season. The need for larger exports comes despite estimates of a smaller crop next season- expectations for larger exports is a reflection of large carry in stocks and the fact that domestic production is still likely to exceed domestic demand.

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more