- Quick take

- 3 March 2020

- Commodities daily

The Commodities Feed: Easing induced rally

Your daily roundup of commodity news and ING views

Energy

Oil markets were part of the broader bounce higher in markets yesterday, with expectations of action from central banks in response to the anticipated effects of the Covid-19 outbreak. US Fed Chairman, Jerome Powell, said late last week that the Fed would use necessary tools to support the economy if needed. Easing from central banks may offer some respite to markets, but ultimately what markets need to see is a peaking in the outbreaks outside China, or at least signs of peaking, to suggest that the worst is behind us.

In China, there are signs already that we are seeing a return to normality. New cases of Covid-19 have dropped dramatically, while if we look at refinery activity, last week, independent refiners in the country increased run rates, suggesting that we are starting to see a recovery in fuel demand. Although admittedly run rates are still well below the levels they were prior to the Lunar New Year holidays.

Key for the oil market outlook will be the OPEC+ meeting in Vienna on Thursday and Friday this week. OPEC+ will need to surprise the market with the level of cuts if they want any chance of pushing prices higher. Clearly a lot has changed over the last month, and trimming output by an additional 600Mbbls/d, as recommended by the Joint Technical Committee is not going to be sufficient.

Sticking with the group, and production estimates for OPEC over February are starting to come through. According to a Bloomberg survey, output for the group averaged 27.91MMbbls/d over the month, down 480Mbbls/d MoM, and the lowest monthly output seen since April 2009. Libya, which is exempt from the production cut deal, was the driver behind the decline, with output falling by 640Mbbls/d MoM, reflecting the impact from the ongoing export blockade in the country. This, as mentioned yesterday, is another factor which complicates the decision for OPEC+, given that it is unknown when Libyan output will return to normal.

Finally, given the scale of the sell-off last week, and the fact that we are heading into a key OPEC+ meeting, we could see a bit more short-term strength in the market, with shorts coming in to take profits ahead of the meeting.

Metals

Gold saw a slight recovery yesterday, although gave back much of its gains as the day progressed. Clearly all this talk of central bank easing is constructive for gold prices and underlines the supportive outlook for the gold market. However, markets will need to see action from central banks rather than just expectations of easing and rhetoric. Meanwhile, despite the sell-off seen on Friday, total gold ETF holdings saw inflows of 277koz on Friday- the third-highest daily number since the start of the year, and taking total holdings to 84.7moz.

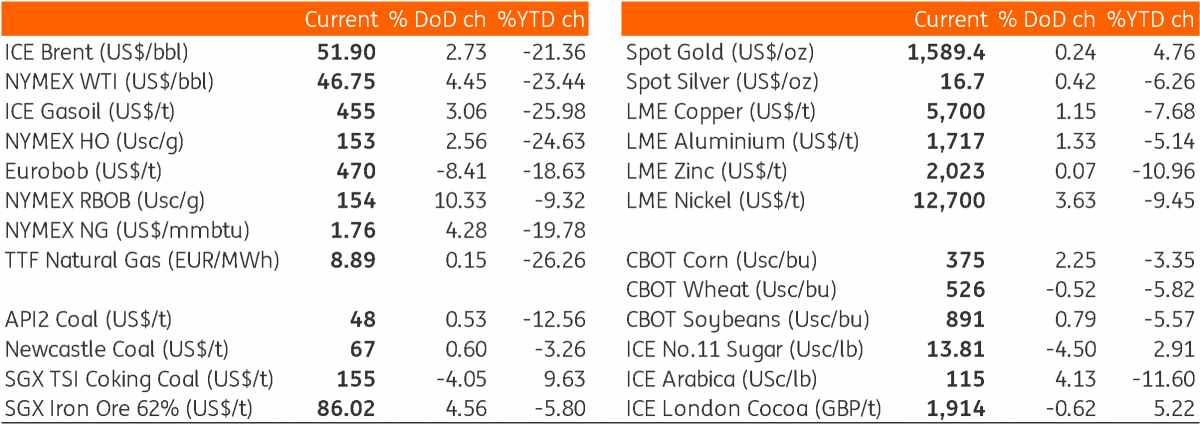

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more