- Quick take

- 30 January 2020

- Commodities daily

The Commodities Feed: Demand worries linger

Your daily roundup of commodity news and ING views

Energy

Yesterday's oil market strength was short-lived, with the rally fizzling out through the day. This trend was briefly interrupted by news that Yemen Houthis had launched a missile attack on a number of targets in Saudi Arabia, including Aramco oil facilities once again. The attack targeted infrastructure in the southern Jazan region - Aramco does not have any crude oil production or export facilities in the region but they do have a 400Mbbls/d refinery in the location. Reports suggest that all missiles were intercepted. Market attention has returned to uncertainties over the demand impact from the Wuhan virus, while also digesting a bearish EIA report. As a result downward pressure on the oil complex has continued this morning.

Yesterday’s EIA release showed that US crude oil inventories increased by 3.55MMbbls over the last week, by more than the market was expecting and very different from the 4.27MMbbls drawdown the API reported the previous day. A key driver behind the larger than expected build was the 3.3 percentage point decline in refinery run rates, which saw crude oil inputs fall by 933Mbbls/d over the week. These lower run rates should offer some relief to refinery margins which have really struggled in recent months. Yet, despite the reduction in utilisation rates, gasoline stocks still increased by 1.2MMbbls - reflecting of the poorer demand seen lately.

Sticking with refined products, it appears there will be little relief for middle distillates in the near term. According to Bloomberg, a preliminary loading plan suggests that diesel exports from the Russian port of Primorsk will jump to 1.75mt in February, equivalent to around 452Mbbls/d, and up from 391Mbbls/d in January. This would be the largest monthly volume seen since at least late 2016. Expectations that IMO 2020 shipping regulations would be bullish for middle distillate cracks has certainly not played out, with the spot ICE gasoil crack trading at around US$10/bbl - down from over US$20/bbl in October.

Finally back to the Wuhan virus, and there is the risk that sentiment gets hit further in the near term. A number of international flights to China have been cancelled and if this trend continues in the coming days and weeks it will likely only deepen demand concerns. In recent days there have been suggestions that OPEC+ might be forced to make further cuts, particularly if the market continues to trend lower. Yesterday there were reports that the Algerian oil minister said that OPEC+ would consider bringing forward their extraordinary meeting planned for early March to February, given current developments. While demand is a real concern, it’s important not to forget about the supply disruptions from Libya - if these losses persist, it would be enough to swing the market into deficit this quarter.

Metals

While broader markets, including metals, tried to recover in early morning trading yesterday, further details on the impact of the coronavirus hit the market and downward pressure resumed on the metals complex. This trend has continued in early morning trading today. As previously mentioned, if we see further travel restrictions, or if the World Health Organization does determine the Coronavirus a global health emergency, this could further hit sentiment.

While the degree of damage to the economy and to metals demand remains unknown, clearly the short term picture has darkened. However, currently low prices should attract some consumer hedging, particularly for those metals which have a more bullish narrative when it comes to fundamentals. Other participants may take a wait-and-see approach for now, at least until there is more clarity or a stabilisation in the number of cases. While the worst of the initial reaction may have passed for markets, clearly the number of cases is still rising and it will be hard for markets to absorb these demand risks. It seems the bulk of China’s semi-fabricators have decided to extend holidays, and are set to only return in the week of 10 February.

Turning to iron ore, and the relief rally in the most active contract on the SGX was short-lived, with prices trading below US$83/t this morning. Once again it was no surprise that virus fears are also weighing on ferrous metals. In terms of supply, Fortescue released its latest quarterly production update today, which showed that the miner shipped 46.4mt of iron ore for the quarter ending in December, up 10% QoQ, and 9% higher YoY. Given strong shipments over the first half of its financial year, the miner expects full year shipments to come in towards the top end of its 170-175mt guide range, compared to 167.7mt shipped in the previous year.

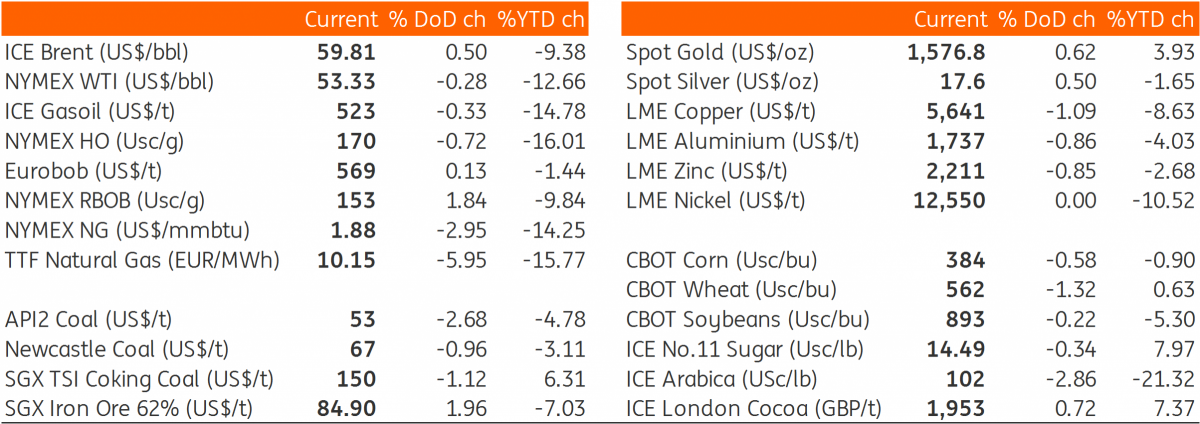

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more