- Quick take

- 10 December 2019

- Commodities daily

The Commodities Feed: Copper settles above US$6k

Your daily roundup of commodity news and ING views

Energy

After deeper than expected OPEC+ cuts boosted oil prices, the market already appears to have moved on, with the outright (flat) price settling lower yesterday, and opening weaker this morning as well. Now with OPEC+ meetings out of the way, the market will likely focus back to trade talk developments, particularly with the 15 December "deadline" fast approaching.

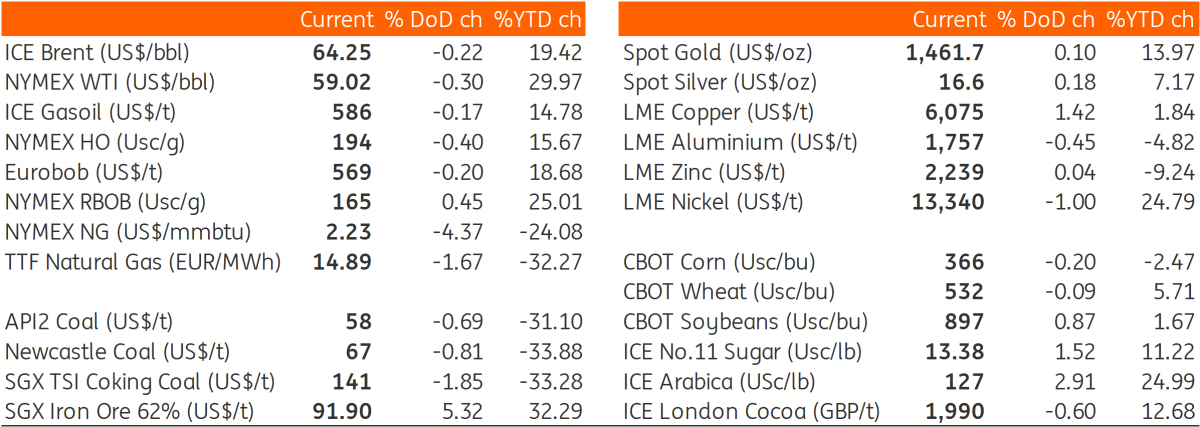

While ICE Brent flat price continues to trade in a range of US$60-65/bbl, time spreads continue to strengthen. The ICE Brent Feb/Mar spread hit backwardation of US$1/bbl, up from US$0.64/bbl at the end of November. This strength continues to tell us that the prompt physical market is tight, and this is aligned with our balance sheet, which shows hefty stock drawdowns over the last quarter of this year. Looking to 1Q20, and following the OPEC+ action, time spreads are also likely to be better supported now, with expectations that the surplus over the period will shrink considerably.

Looking ahead to the rest of the week, there are a number of relevant data releases. Today we will get the usual API numbers for US oil inventories. Expectations are that crude oil stocks in the US declined by 2.5MMbbls according to a Bloomberg survey. We should continue to see refinery run rates edging higher, which supports the idea of a crude oil draw. This will be followed by EIA numbers on Wednesday. Meanwhile, on Wednesday, OPEC releases its monthly oil market report, which will include production estimates for November alongside supply & demand forecasts for 2020. Finally, on Thursday, the IEA will release its monthly oil market report, and the market will be keen to see if the agency thinks that OPEC+ has done enough to eat away at the surplus over 1Q20.

Metals

Having been largely rangebound for much of 2H19, copper has been looking for a break higher, given its relatively more constructive fundamentals (mainly supply-side developments). Yesterday LME copper managed to do this, settling above US$6,000/t, and reaching levels last seen in July this year. There are a number of drivers behind this latest move.

- Firstly, last Friday, China said that it would waive tariffs on imports of soybean and pork from the US. Since then there have been reports that Chinese buyers bought at least five bulk cargo shipments of U.S. soybeans after Beijing provided at least 1mt in new tariff waivers. This is sending a positive message to the market ahead of the December 15th deadline for tariff hikes. Clearly the market is anticipating a positive outcome to the phase one deal. The risk is that negotiations fail and further tariffs are imposed on the 15 December.

- Secondly, last week's China Central Economic Conference sent a key message that Beijing vows to maintain economic growth in a reasonable range and strengthen infrastructure investment growth. This has added fresh hopes to copper demand.

- Thirdly, LME inventories have been in a downward trend. After hitting an intra-year high of 338kt at the end of August, stocks have fallen by 43% to just 191kt on Monday.

- Finally, last week's release of China’s scrap import quota has turned out to be a bit disappointing, which suggests that short-term scrap supply is likely to remain tight in China.

These factors combined have outweighed some less promising indicators, such as weaker US ISM manufacturing data and China exports. That said, the most recent rally is largely driven by hope for a trade deal and future demand. We have yet to see any substantial improvement in physical demand. As we approach the trade tariff deadline this Sunday, trade-related headlines over the remainder of the week will remain key for market sentiment. If tariffs were to get delayed, the market may still take this as a positive sign, as it would suggest that both sides are still working towards a deal. For more on this, read the latest from our Chief Economist in Asia.

Turning to precious metals, palladium prices have continued their surge, and the palladium/platinum price ratio has hit a fresh high of 2.11. This stellar performance is deeply rooted in its market deficit this year, which has exceeded market expectations. Palladium's strength has been driven by stronger demand from the auto industry, as stricter emissions regulations have increased loadings in auto-catalysts. Meanwhile, supply remains fairly inelastic, and it is hard to see a quick response in the imminent future. This is because palladium supply is usually a by-product of other mining activity, and also because supplies are concentrated in Russia and South Africa, with labour-related issues in the latter limiting further investment.

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more