- Quick take

The Commodities Feed

- 18 October 2018

- Commodities daily

Your daily roundup of commodities news and ING views

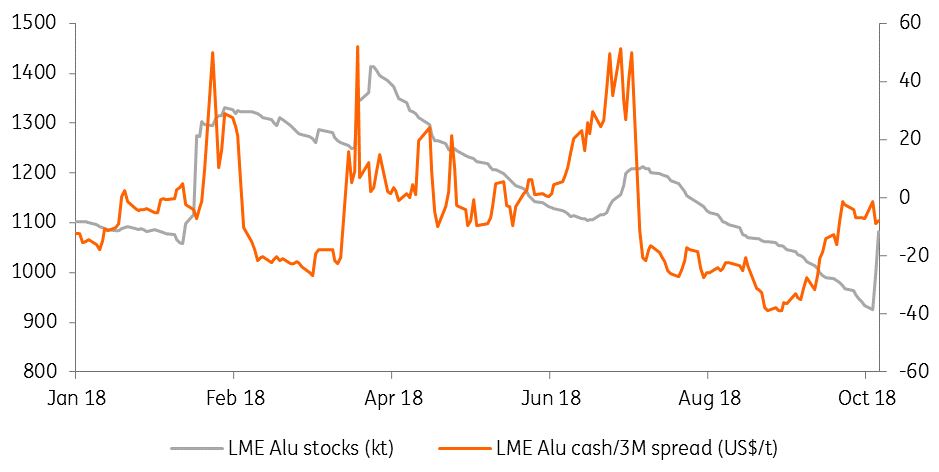

Chart of the day: LME Aluminium inventories vs. cash/3M spread

Energy

US crude oil inventories: The EIA surprised the market yesterday, reporting that US crude oil inventories increased by 6.49MMbbls over the last week, much higher than the 2.5MMbbls build the market was expecting. The larger than expected build was driven predominantly by lower crude oil exports, which fell by 794Mbbls/d over the week, with flows likely impacted by hurricane activity last week. Meanwhile, crude oil production in the Lower 48 fell by 300Mbbls/d, also reflecting disruptions dues to Hurricane Michael.

WTI spreads continue to weaken: WTI nearby time spreads continue to weaken, and yesterday’s EIA report certainly did not help, with Cushing stocks increasing by 1.78MMbbls. The WTI Dec/Jan spread has fallen from a backwardation of $0.31/bbl in mid-September to a discount of $0.05/bbl, and this move does correspond fairly well with the large inventory builds that we have seen in the US since mid-September. The recent builds we have seen in the US have also weighed on the WTI-Brent spread, with the discount widening to more than $10/bbl yesterday.

Metals

Gold ETF holdings keep growing: Investors continued to add to their ETF holdings in gold, with total holdings increasing by 839kOz to total 67.9mOz. Gold has reappeared as a safe haven asset, with stock market jitters, trade tensions and political worries concerning investors. The FOMC meeting minutes may weigh slightly on gold in the immediate term, with the minutes showing general agreement for further rate rises moving ahead.

LME aluminium stocks: Aluminium inventories in LME warehouses have bounced back above 1mt, with 156.5kt of the metal added over the last two days, all of it into Asian warehouses. Over the previous three instances of inventory increases this year, the LME cash/3M spread did see wild swings, however up until now, the spread has been fairly flat.

Agriculture

German sugar production estimates fall: German industry body WVZ now expects that German sugar production over the 2018/19 season will fall to 4.41mt, down from their previous estimate of 4.47mt. This is also quite a bit lower than the EU Commission estimate of 5.16mt produced over the 2017/18 season. Concerns over the EU crop as a whole, due to dry and hot weather conditions over the summer, have been supportive for the white sugar market, with the March whites premium trading at around $75/t.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more