- Quick take

- 24 April 2019

- Commodities daily

The Commodites Feed: Spread strength & oil market tightness

Your daily roundup of commodity news and ING views

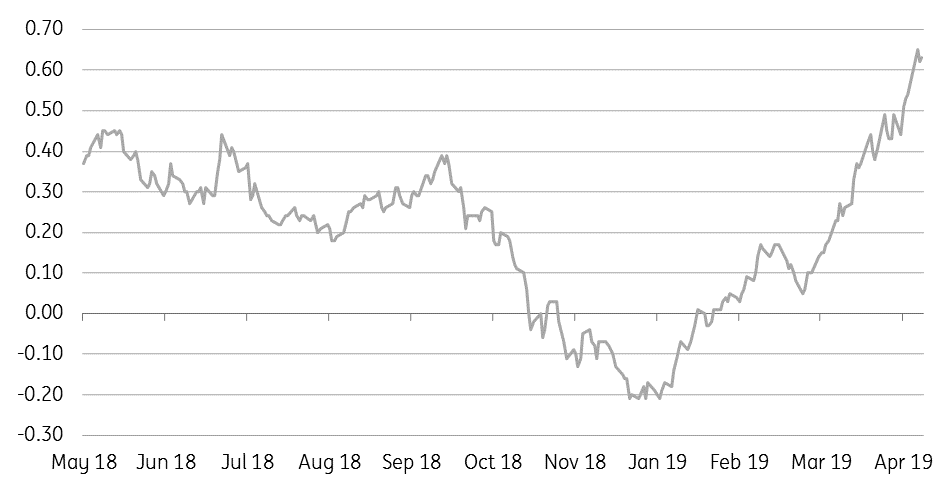

ICE Brent Jun/Jul spread strength (US$/bbl)

Energy

Spread strength & market tightness: Brent time spreads continue to move deeper into backwardation, with the front month, Jun/Jul spread hitting US$0.65/bbl earlier this week. The strength in the spread reflects both a tightening balance as a result of OPEC+ cuts, as well as the view that the market will tighten further following the US announcement that it will end Iranian oil waivers. The biggest uncertainty for the market is how quickly the Saudis respond to any supply shortfall from Iran. Taking too much of a reactive approach not only risks political pressure from the US and oil importing countries but also increases the risk of demand destruction, particularly in a strong US dollar environment.

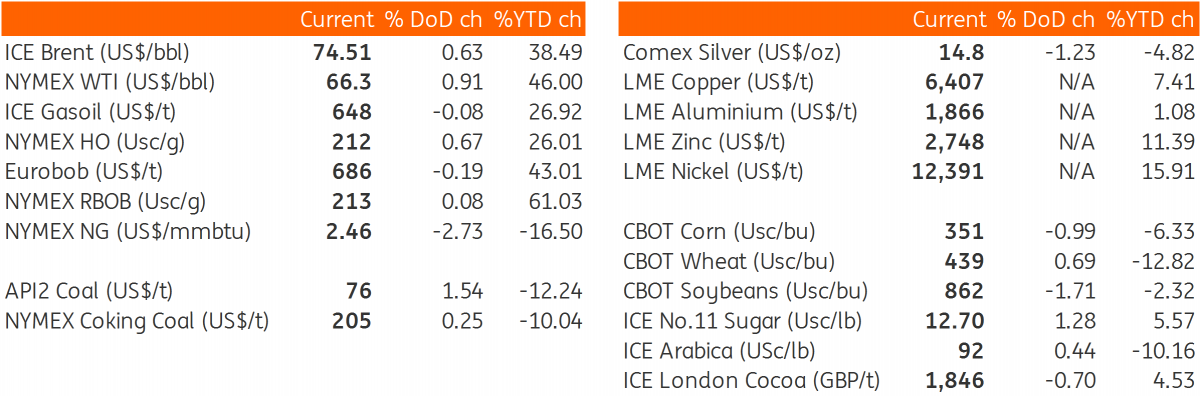

US crude oil inventories: The API reported yesterday that crude oil inventories in the US increased by 6.86MMbbls, compared to market expectations of a 1MMbbls build. The API also reported a surprise build of 2.16MMbbls in gasoline, and a 865Mbbls draw in distillate fuel oil. The more widely followed EIA report will be released later today, and if these numbers are similar to API numbers, we could see some downward pressure on prices, with builds in both crude and gasoline.

Metals

Aluminium supply: The latest data from the International Aluminium Institute shows that global aluminium output declined 0.5% month-on-month (-0.1% year-on-year) to 174.6kt per day in March, with production falling in Western Europe, Asia ex-China and North America. Chinese aluminium output was largely flat at 99.1kt per day. Global aluminium production was down 1.4% quarter-on-quarter to average 174.9kt per day in 1Q19 as weaker aluminium prices and shortages of alumina have weighed on output. Earlier, Chinese customs data showed that China remained a net importer of alumina for the second consecutive month, with Chinese domestic prices remaining at a premium to international prices. Over 2018, China turned to a net exporter of alumina, helping to fill the shortfall in the ex-China market.

Gold weakness: Gold prices remain under pressure this month, falling nearly 1.7% since the start of April, and more than 5% from the recent peak of US$1,341/oz in February. Positive equity markets and optimism over trade war talks has weighed on the demand for safe-haven assets. ETF investors have offloaded nearly 2mOz of gold holdings over the past three months reflecting a move towards riskier options. CFTC data also shows that speculators over the last reporting week sold 59,706 lots in COMEX gold, which saw them switch back to holding a net short for the first time so far this year. Money managers held a net short of 3,969 lots as of last Tuesday.

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more