- Quick take

- 25 April 2019

- Turkey

Turkey: The CBT remains on hold at its April meeting

At the April MPC, the CBT kept the policy rate flat at 24%, in line with consensus. It dropped any reference in the statement to deliver further monetary tightening, if needed.

| 24% |

1-week repo rate(Unchanged) |

| As expected | |

At its April rate-setting meeting, the CBT remained on hold. The policy rate (1-week repo rate) remained unchanged at 24%, in line with consensus.

In the statement the CBT kept one of the two key sentences - remaining committed to maintaining a tight monetary policy stance until there is a significant improvement in the inflation outlook. However, contrary to expectations that it could be more hawkish in its guidance, the bank dropped any reference to its determination to deliver further monetary tightening if needed.

On the one hand, the removal of the tightening bias means the CBT sounds less hawkish against a backdrop of macro uncertainties and currency volatility, with heightened risks of inflation. In March annual inflation was flat while core inflation maintained its downtrend - the bank cites higher food and import prices along with elevated inflation expectations as the major risks to price stability. We think inflation inertia and FX pass-through would be key for the inflation outlook in the period ahead, though the current economic backdrop - with ongoing weakness in domestic demand and base effects - will remain supportive. The TRY responded negatively, moving from around 5.90 vs USD to 5.95 after the announcement .

On the other hand, the CBT specifies that the “monetary stance will be determined to keep inflation in line with the targeted path”. This does not rule out the possibility of a tightening, with further risks of inflation and downward pressure on the currency.

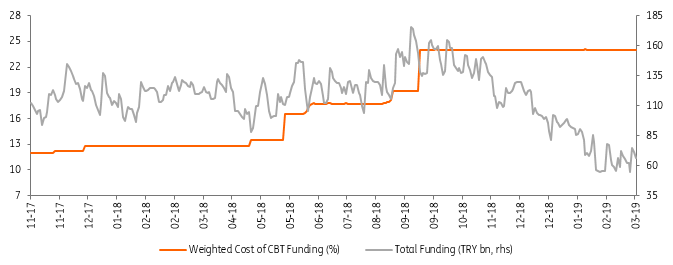

Central Bank Funding

The remainder of the statement was broadly unchanged. According to the CBT economic activity remains subdued on the back of tight financial conditions, with a continuation of the rebalancing trend. The bank sees ongoing relative external demand strength while expecting further improvement in the current account balance.

So the CBT has unexpectedly revised its policy guidance and dropped its tightening bias. However, given a still fragile currency, continued dependence on external financing despite recent improvement in external imbalances and ongoing inflationary risks as indicated by elevated core and services inflation, we do not expect a rate cut in the first half of the year. Depending on TRY performance, a moderate monetary easing may be on the agenda in the second half of the year, likely in the fourth quarter.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more