- Quick take

- 6 March 2019

- Turkey

Turkey’s central bank: Still in wait-and-see mode

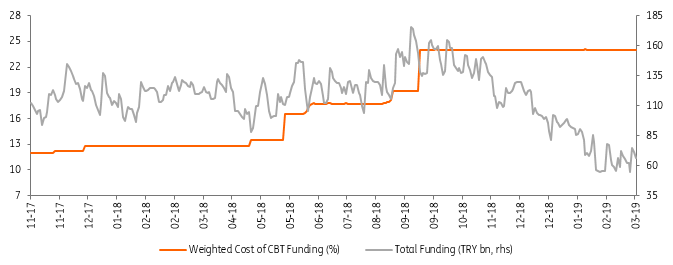

The central bank of Turkey kept the policy rate unchanged at 24% and maintained its hawkish bias given the fragility of the currency and ongoing inflationary pressures. We expect the Bank to maintain its tight stance until there is a visible improvement in the inflation outlook with potential modest cuts likely in the second quarter

| 24% |

1-week repo rate(Unchanged) |

| As expected | |

At the March meeting, the central bank of Turkey kept the one-week repo rate unchanged at 24%, in line with the consensus, despite the downtrend in annual inflation in February showing the impact of relatively benign food prices, after a spike in January and seasonality in clothing, despite higher energy inflation.

The decision created a minor impact on the exchange rate with the USD/TRY dropping to 5.36 and then recovering rapidly to above 5.40.

So far, the central bank has shown no signs of complacency and has recently come up with strong wording, promising to maintain a policy that reduces inflation to single digits in the least possible time.

This stance shows the Bank’s sensitivity to ongoing inflation challenges with continuing upside risks, due to deteriorating expectations and a fragile outlook for the lira, given geopolitical issues and the upcoming elections.

Accordingly, the Bank stayed on hold again this month, while keeping its hawkish bias with a promise to deliver policy tightening if required, until the disinflation trend becomes more pronounced.

Central bank of Turkey funding

The accompanying statement includes minor changes compared to the previous month.

One addition to the statement is related to the external demand as the bank mentions “relative” strength while in January the sentence was “external demand maintains its strength”.

For economic activity, the central bank revised its assessment to “economic activity displays a slow pace” from “slowdown in economic activity continues”. These changes don't signify a meaningful shift in the Bank’s assessment since January. On the inflation side, the Bank acknowledges the improvement with the support of “import prices” and “domestic demand conditions”, though remains vocal about prevailing risks on price stability.

The central bank remains sensitive to price and financial stability risks and kept its hawkish bias given the fragility of the currency, continued dependence on external financing despite recent improvement in external imbalances and ongoing inflationary risks, as indicated by elevated core and services inflation.

The Bank will maintain a tight stance until there is visible improvement in the inflation outlook to gradually restore credibility with potential modest cuts likely in the second quarter.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more