Taiwan’s May inflation edged higher but stable core inflation should keep rates on hold

Headline CPI edged up to 2.2% year-on-year amid pressure from food, electricity, and healthcare prices, but stable core inflation means the Central Bank of China will not feel pressure to further hike rates

| 2.2% |

Taiwan's May CPI inflation (YoY) |

| As expected | |

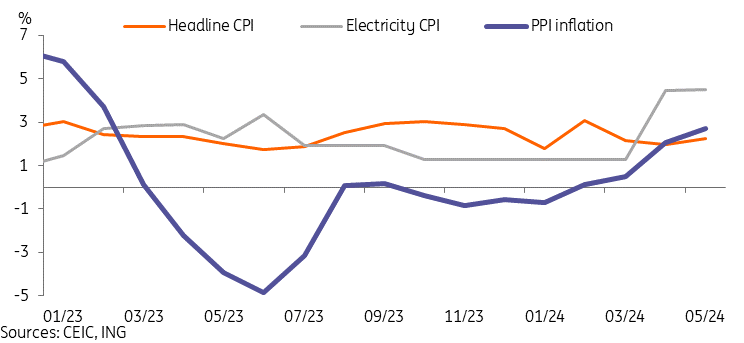

Electricity prices and PPI have outpaced headline inflation since April price hike

Headline CPI trended higher while core CPI stabilised

Taiwan’s May inflation data mostly came out in line with our expectations. Headline CPI inflation edged up to 2.2% YoY from 1.95% YoY in April, a little higher than our forecast for 2.1% YoY. Core CPI, on the other hand, was broadly unchanged at 1.8% YoY, coming in a little cooler than market forecasts for 2.0% YoY. PPI inflation rose to 2.7% YoY, up from 2.1% YoY in April.

Looking at the components of inflation, as expected, the April electricity price hike continued to play a role in the inflation trajectory. The electricity component of CPI and PPI inflation in May rose by 4.5% and 4.2% YoY, respectively, both well above headline levels.

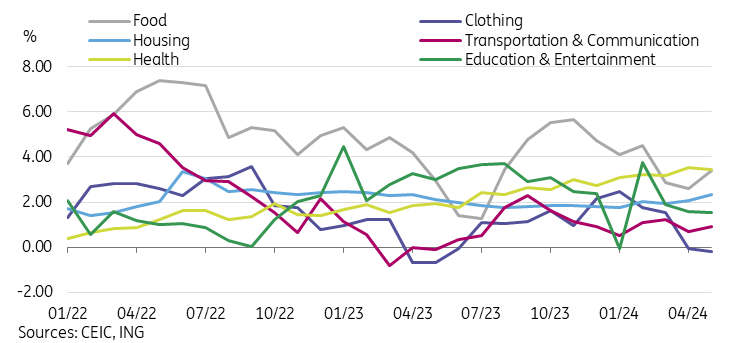

The other key contributors to CPI inflation included food prices, which grew by 3.4% YoY, and healthcare prices, which rose 3.5% YoY.

Most other subcategories were below or near the 2% inflation target, and clothing prices actually fell slightly further into deflation at -0.2% YoY. Overall, the core inflation number indicates that inflationary pressure seems to be under control for now.

Inflationary pressure has been concentrated only in a few categories

Inflation could remain above target for a few more months but no further hikes expected

Moving forward, we are expecting inflation to remain above the 2% target for several months, primarily considering the base effect but also taking into account the possibility of some spillover effect from the electricity price hike to other categories of inflation starting to take effect.

Given the broadly unchanged core CPI inflation, we do not expect this month’s CPI release to apply any pressure on Taiwan’s Central Bank of China (CBC) to consider further tightening at next week's monetary policy meeting despite the headline inflation number moving a little higher.

In our baseline case, although we anticipate inflation to trend higher in the next several months, the overall inflationary pressure is not expected to be significant enough to cause the CBC to implement another rate hike in the next several months, especially with global central banks starting rate cuts this month. At the same time, it’s also unlikely to see the CBC pivot toward rate cuts before the Federal Reserve makes its first move, barring an unexpected and significant deterioration of economic fundamentals. We continue to see a cut rather than another hike as the likelier route, with potentially the first cut coming toward the end of the year or early in 2025.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap