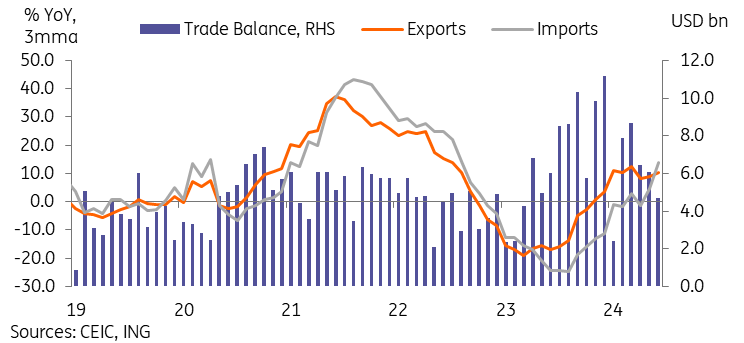

Taiwan export and import growth surge to 28-month highs in June

Export and import growth both far exceeded forecasts in June, reaching their highest levels since February 2022

| 23.5% YoY |

Taiwan export growth |

| Higher than expected | |

Export and import growth hit 28-month highs amid a broader recovery and supportive base effects

Taiwan's trade data came in much stronger than forecast in June, with exports surging 23.5% YoY and imports up 33.9% YoY, eclipsing both the market and our forecasts. In terms of the impact on GDP growth, the net impact was a smaller trade surplus of only USD4.7bn, lower than forecasts.

As expected, machinery and electrical equipment (up 32.8% YoY) continued to lead export growth. Minerals (23.8%), chemicals (15.4%), plastics (9.2%), and textiles (16.5%) recovered in June, after recording negative growth for the first five months of the year.

Exports to other regions finally recovered in June, after previously being concentrated in North and Central America. Export growth to the US (74.2%) continued to lead the pack and exports to ASEAN (30.9%) continued to register strong growth. We also saw a recovery of exports to Mainland China & HK (7.3%) as well as to Europe (7.4%), helping to bolster overall export numbers.

Import growth surprised by even more than export growth in June. The numbers showed broad-based strength, with most categories seeing significantly higher growth in June than in previous months. The largest import categories - machinery & electrical equipment (up 37.7% YoY), mineral products (33.9%), and base metals (58.9%) - which together represent over two thirds of all imports in the first half of 2024, all surged in June. Imports from the US grew by 41.9%, while imports from Mainland China and Hong Kong grew by 35.1%.

Taiwan's trade growth surged but the trade surplus came in lower than forecast

Base effects should continue to support YoY growth numbers in coming months

There are significant base effects in play so the data should still be taken with a grain of salt. Market forecasts unanimously expected a rebound in the data in June as base effects from 2023 heavily favoured a strong year-on-year read. In June 2023 exports fell by -23.4% YoY while imports fell by -30.2% YoY, both the largest YoY declines of the year.

Moving forward, export and import growth should moderate from June's extraordinarily strong read. Year-on-year numbers should remain well supported for most of the second half of 2024. More importantly for growth will be how the trade surplus develops, and if we can see a sustained broader recovery in non-semiconductor related export categories.

In general, and with recent economic data trending stronger than expected amid the semiconductor boom, we have upgraded our 2024 GDP growth forecast to 3.8% YoY.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap