Achieving the deficit target in Hungary has improved

June brought another low monthly budget deficit, but with new government measures announced, we believe that the previously calculated 0.0-0.5ppt slippage risk to the 4.5% deficit target is largely covered

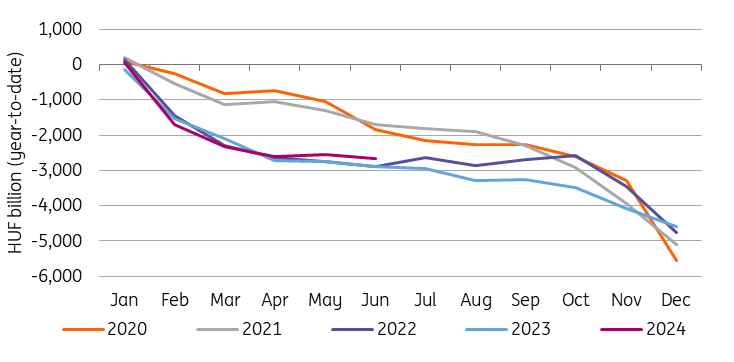

The monthly budget deficit was HUF108bn in June, bringing the year-to-date (YTD) general government cash flow deficit to HUF2.66tr. This means that the shortfall has reached 67% of the Government Debt Management Agency’s planned financing needs for 2024. June’s deficit was the lowest monthly shortfall we’ve seen for the sixth month in 22 years, which is a positive sign. Given that most expenditure tends to be front-loaded (notably interest payments on retail bonds), this means that the bulk of the expenditure is likely to be behind us, increasing the chances of achieving the 4.5% of GDP deficit target.

Budget performance (year-to-date, HUFbn)

The Ministry of Finance's statement provided some information on the specifics of the deficit structure. In this regard, as usual interest expenditure was once again highlighted with an outflow of HUF2tr in coupon payments YTD. Based on our calculation, this means that coupon payments amounted only to around HUF249bn in June, which we believe is likely to be significantly skewed towards retail bond payments to households. With the vast majority of coupon payments to households due in the first half of the year (approximately 80%), we believe that the pressure on the expenditure side from this particular item is likely to ease in the coming months.

Pension expenditure was also highlighted with YTD payments of HUF3.22tr, which according to our calculation means that payments in June amounted to HUF378bn. In this regard, unlike retail coupon payments, this particular item on the expenditure side is roughly evenly distributed over the year as a whole.

Last but not least, the Ministry pointed out that expenditures on EU-funded programmes increased by HUF144bn in June, while revenues from the EU increased by only HUF32bn. This means that the gap between these two budgetary items has increased even further from May to June, reaching a monthly deficit of HUF112bn. In this regard, it seems like pre-financing of EU projects are still ongoing, as expected, but we think that uneasy relations between Budapest and Brussels continue to create a bottleneck in EU transfers and this gap will not narrow materially during 2024.

New measures taken by the government to help cover slippage risk

We have long argued that there is a slippage risk in the 2024 budget, which we have previously calculated at around 0.0-0.5 percentage points of GDP. However, with today's budget-related announcements, it appears that the government has addressed the issue head-on by announcing new austerity measures. In this regard, the cabinet minister has announced that the government will levy a "defense contribution on the wartime windfall profits of multinationals".

In reality, some of the measures will target those banks that haven't increased the proportion of Hungarian government bonds in their portfolios, which was the government's intention last year. In addition, the transaction tax on banks will be raised, while a new tax will be levied on FX transactions. At the same time, contrary to previous commitments, the windfall profits tax for energy companies, multinationals and retailers will not be reduced in 2024. To have a comprehensive analyses and market-related impact assessment, we have to wait for the details of the new measures.

According to the government's calculations, the expected additional revenue from these announcements is around HUF400bn, or around 0.5% of GDP. This basically means that our calculated slippage risk for 2024 could be covered by these new measures alone. Moreover, if macroeconomic conditions improve as expected in the second half of this year, the VAT revenue stream could further increase the government's room for manoeuvre.

If there is any headroom, we believe the government will try to use it to implement new spending programmes to boost consumption ahead of the 2026 elections. As a result, we do not expect the deficit to fall below 4.5% of GDP at the end of the year, even though improving macroeconomic conditions might signal a lower deficit. We still expect the 2024 deficit to be between 4.5% and 5.0% of GDP, with a preference for the higher end given the government's recent track record.

Finally, the newly announced measures will not only help the 2024 budget, but also next year's budget. In our view, the existing windfall taxes will not be abolished at the end of this year, while the newly announced measures are likely to remain in place. All in all, this means that we are one step closer to achieving next year's current deficit target of 3.7% of GDP, although our forecast is for a deficit of 4.2% of GDP in 2025.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap