- Quick take

- 24 October 2019

- FX Sweden

Swedish Riksbank keen to exit negative rates, despite weaker outlook

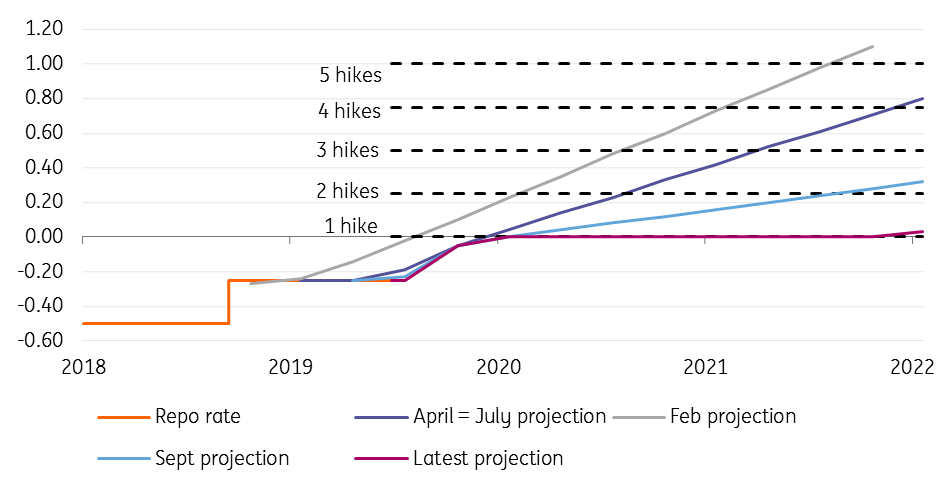

The Riksbank is sticking to its December rate hike amid a deteriorating economic backdrop, signaling a clear willingness to exit negative rates. Policymakers have said rates could fall again if the outlook worsens, but this latest guidance coupled with a more relaxed attitude towards the risk of SEK appreciation, suggests a high bar for easing

The Swedish central bank has caught markets by surprise by reiterating that rates will most likely rise later this year. The Riksbank has said that rates will “most probably” rise to 0% in December. Probably the biggest takeaway from this is that it suggests a clear willingness to exit negative rates. The domestic and global economic backdrop has deteriorated significantly over the past few months, which suggests little impetus otherwise to increase interest rates.

Our base case is that rates will rise in December, but will remain on-hold thereafter

We had expected the Riksbank to push back the timing of the next hike. The PMIs are now below the breakeven PMI level, while there are signs that the jobs market is slowing – albeit as the central bank emphasises, the latest labour data signalling a sharp spike in unemployment potentially contains quality issues.

We are also cautious about the forthcoming wage negotiations, and whether they will translate into upward pressure on wages, given that inflation expectations among labour organisations are slipping. The Riksbank has marginally lowered its pay growth projections in its latest report.

All of this means the Riksbank is now signalling no additional rate hikes after December, compared to one previously. We agree with this assessment too. While policymakers have suggested they could cut rates again should the economic outlook worsen, today’s decision suggests the bar for doing so is set relatively high.

Don’t forget that policymakers are much more relaxed about the risk of currency strength amid ongoing SEK weakness, which indicates the central bank will be in no hurry to follow in the footsteps of dovish central banks overseas.

Our base case is that rates will rise in December, but will remain on-hold thereafter.

After one in December, policymakers don't expect any further rate hikes

'One and done' rate hike set to have limited effect on SEK

All of this is a short-term positive for the Swedish krona (SEK) - the best performing G10 currency this morning. However, we sill think SEK upside is limited.

The domestic economy is slowing, there is uncertainty about the global growth and trade outlook (making a small open economy like Sweden vulnerable). The extent to which the upcoming hike (if delivered) is perceived by the market as a policy mistake (i.e. tightening into a downturn, reminding us of the ECB rate hikes under President Trichet back in 2011), the positive effect on SEK is unlikely to be long-lasting

At this point, the market is pricing around a 50% probability of a rate hike in December and 90% probability by March. This also suggests the boost to SEK from the Riksbank’s tightening may be limited form here – particularly when the central bank is signaling a “one and done” type of rate hike, which may be coupled with dovish language when eventually delivered.

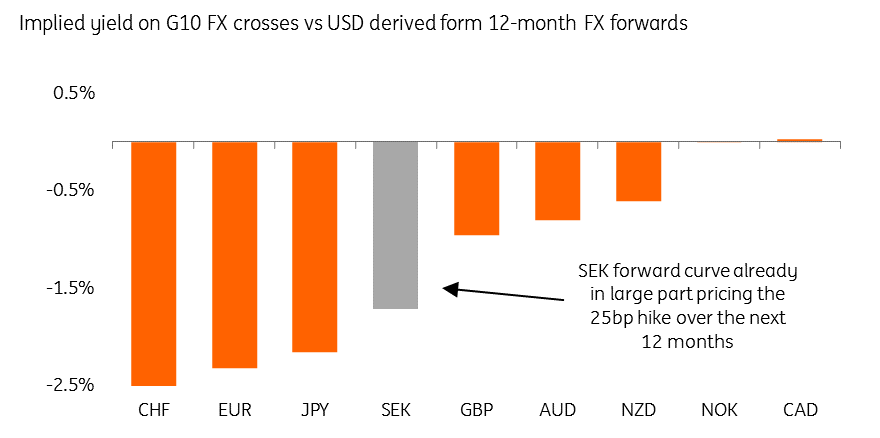

While bringing interest rates out of negative territory is positive for SEK, the currency will still have the lowest interest rate among its higher beta G10 peers (Figure 2), lagging NOK as well as CAD, AUD and NZD. This means that in relative terms SEK is still not overtly attractive – it still is the low yielder with a high beta.

Figure 2: SEK to still show the lowest implied yield among its high beta peers

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more