- Quick take

- 29 June 2023

- FX Sweden

Swedish Riksbank hikes rates and lifts bond sales amid krona weakness

Sweden's central bank has slowed the pace of rate hikes as it walks a fine line between bolstering the ailing krona and avoiding more damage to the fragile housing market. We think another hike is likely in September, but that might be the last

Authors

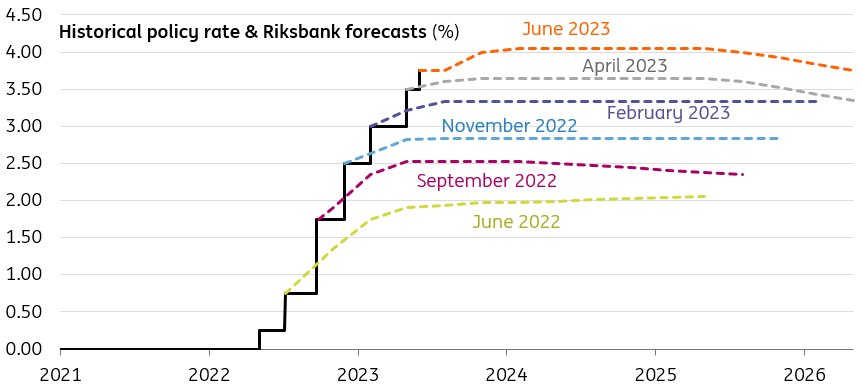

Sweden’s central bank has hiked rates by another 25 basis points amid ongoing concerns about the weak krona. On a trade-weighted basis, SEK is roughly 3% weaker than the Riksbank had been predicting for the second quarter on average in its last set of forecasts from April.

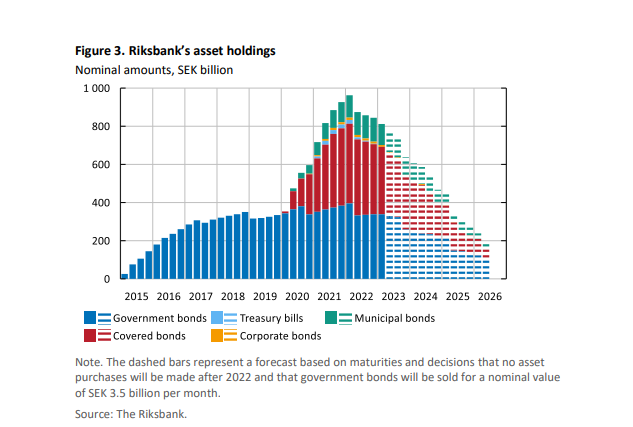

On paper, there’s nothing hugely surprising about today’s decision, though repeated warnings about currency weakness from Governor Erik Thedeen meant there was a tail risk of another 50bp hike this month, not least because the Riksbank meets only twice more this year. That said, the central bank has opted to increase the pace of its sales of government bonds, from SEK3.5bn a month to 5bn, and by the Riksbank's own admission, this is partly designed to help support the krona.

Unsurprisingly those concerns about a weaker currency, coupled with some resilience in both economic activity and house prices, have also led the committee to upgrade its assessment of future rate hikes. The bank is now forecasting one more hike later in the year, and a 20% chance of another, which would take the policy rate to 4.25%. Unlike at the last meeting, there appears to have been no disagreement on the policy decision among the committee.

Riksbank policy rate forecasts over time

On that basis, there’s little reason to doubt that the Riksbank will go ahead with another rate hike at its September meeting. But ultimately Swedish policymakers face a growing trade-off between hiking to bolster its ailing currency, and avoiding a deeper correction in the housing market. Sweden has a much higher share of variable rate mortgages than its peers across Europe, and that means the pass-through from higher rates has been more rapid.

That said, the Riksbank is forecasting another 7% fall in house prices, on top of the 15% we’ve already seen from the peak. In other words, some further pain is already baked into its latest rates projection.

In short, we expect a rate hike in September, but if the Fed and ECB have paused rate hikes by the fourth quarter, then the Riksbank might be content with keeping rates on hold in November.

Unclear what quicker quantitative tightening means for the krona

EUR/SEK has been volatile in narrow ranges after the Riksbank’s announcement today. The positives for the krona are that today’s decision to hike was unanimous and that future rate hikes are promised. What is less certain is what today’s announcement of accelerated quantitative tightening (QT) means for the krona.

Recall that back in February the Riksbank announced that it would be shrinking its holding of assets from around SEK800bn to SEK200bn over the next three years. In April, It started reducing its holdings of nominal and inflation-linked government bonds by SEK3.5bn per month. Today it has announced that the pace of sales will increase to SEK5bn per month starting in September.

The Riksbank argues that its bond sales will raise yields on government bonds while having little impact on lending and deposit rates. It also argues that by supplying these government bonds back to the market, greater liquidity here will attract foreign investors and support the krona.

The hypothesis of QT supporting the krona seems to be untested. So far this year, 10-year Swedish Government Bond (SGB) yields have only traded in a +/- 15bp range against 10-year German Bunds – and serves as a reminder that the ECB is also shrinking its balance sheet at the same time.

In all, we suspect that EUR/SEK can stabilise around the current 11.70-11.80 levels. However, with the real estate market proving to be Sweden’s Achilles heel, we doubt that a sustained recovery in the undervalued krona will emerge until much later in the year when there are clearer signs of improvement in global inflation trends. Until that point, domestic risks in Sweden will continue to see the krona trade on a fragile footing.

Riksbank's initial planned sales of government bonds

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more